Investing & Trading

- TA Notes

- Pivot points, market structure & the three phases of major trends

- Supply & Demand, and Support & Resistance

- 1.3 - Reversal patterns, trend lines & channels

- 1.4 - Volume analysis, Wyckoff techniques & On-balance Volume

- 1.5 - RSI Divergence as a leading Indicator

- 1.6 - Fibonacci & retracement zones

- 1.7 - Candlestick & Pattern Analysis

- Index Confirmation

- Psychology & the Principle of Markets Discounting Everything

- Risk to reward, trade planning & risk management

- Term 1 Masterclass

- Complex divergence

- Hidden Divergence

- Directionally aligned divergence

- Pattern recognition for confluency

- Moving averages, SMA & EMA

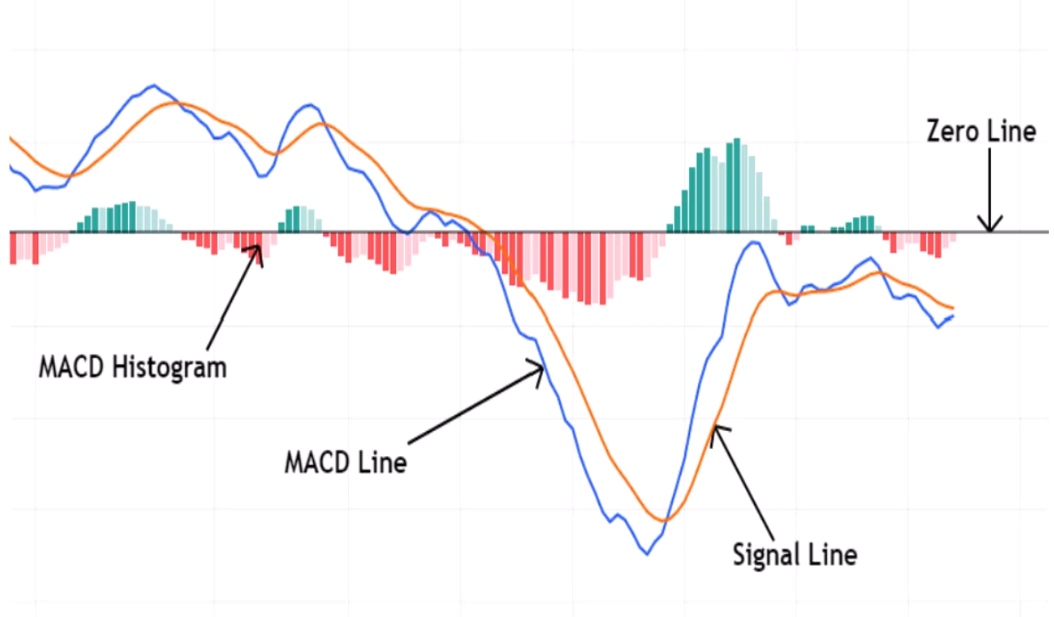

- MACD

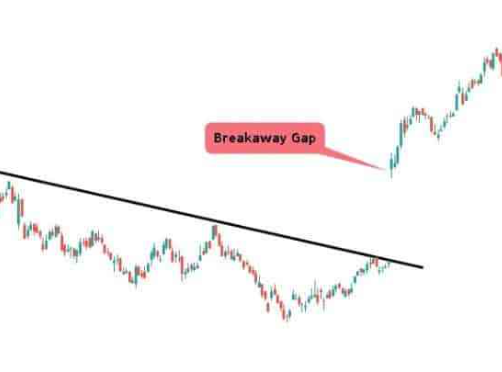

- Gaps

- Market Breadth

- Sentiment analysis

- Fibonacci extensions

- 2.10 - Fibonacci clusters & extension channels

- Term 2 master class

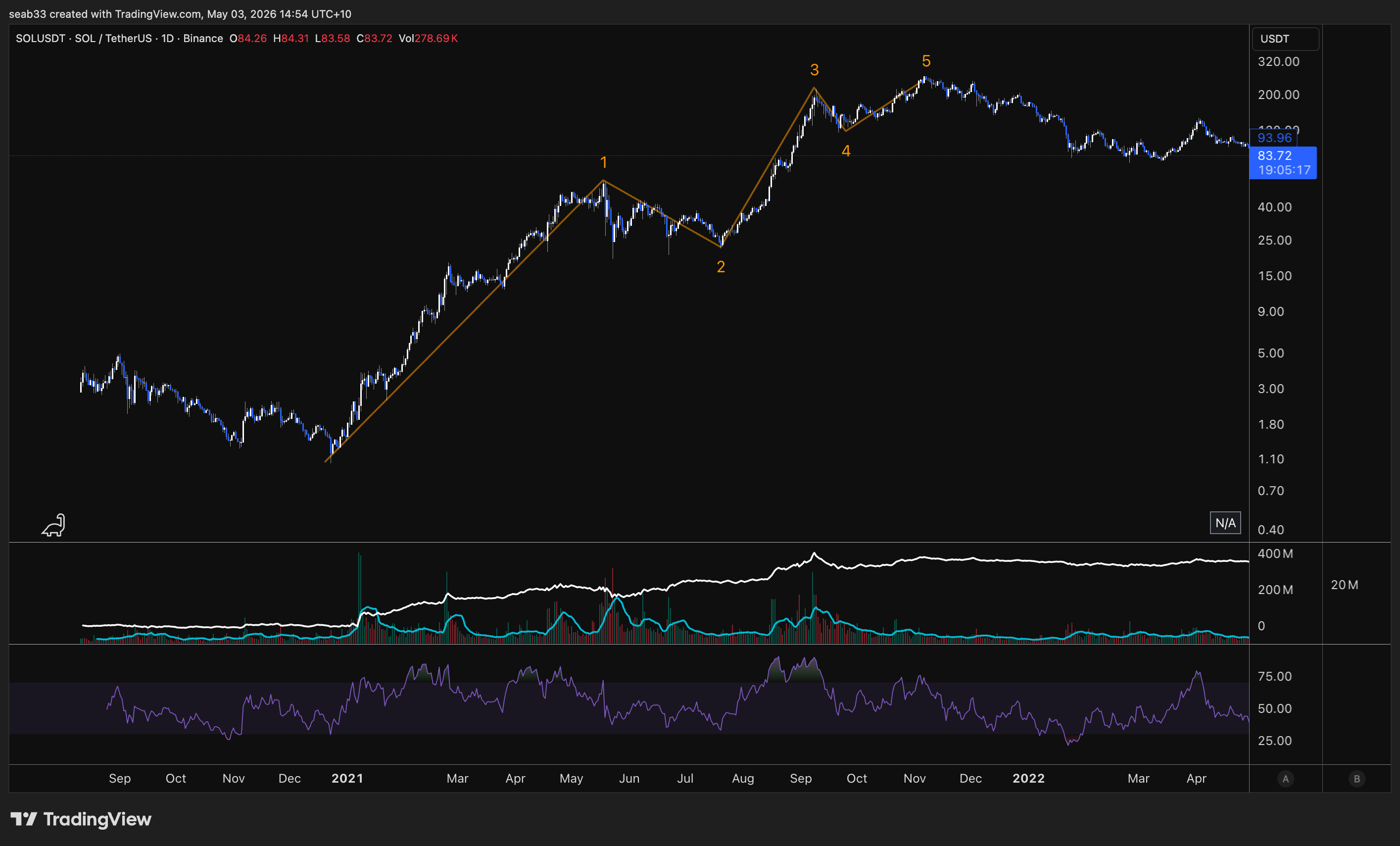

- Elliott Wave - General

- EW notes

- Elliott Wave — Impulse Waves

- Elliott Wave — Extended Waves

- Elliott Wave — Diagonal Waves

- Elliott Wave — Corrections: Zigzags

- Elliott Wave — Corrections: Flats

- Elliott Wave — Corrections: Triangles

- Elliott Wave — Complex Corrections: Double Three (WXY)

- Elliott Wave — Complex Corrections: Triple Three (WXYXZ)

- Elliott Wave — Trading Strategies

- Elliott Wave — Market Psychology & Trading Mindset

- ASX Trader (Dave) - Trade analysis

- Fundamental Analysis Course

- Module 1: The Lassonde Curve & The 10 Stages of a Mining Company

- Module 2: JORC Code & The Resource / Reserve Hierarchy

- Module 3: Ore Grades, Cut-Offs & What "Good" Actually Looks Like

- Module 4: Reading Drill Result Announcements

- Module 5: Economic Studies (Scoping, PFS, DFS)

- Module 6: Capital Structure, Dilution & The Share Register

- Module 7: Catalysts & The Catalyst Calendar

- Module 8: Red Flags, Green Flags & Sneaky Tactics

- Module 9: Macro Overlay — Commodity Cycles & The ASX Small-Cap Resource Cycle

- Module 10: Putting It Together — The "FA Story" and TA Confluence

- Company Fundamental Analysis

- PC Gold Ltd (ASX: PC2)

- Elevra Lithium Ltd (ASX: ELV)

- Galan Lithium Ltd (ASX: GLN)

- Solstice Minerals Ltd (ASX: SLS)

- Minerals 260 Ltd (ASX: MI6)

- Bison Resources Ltd (ASX: BSR)

- Torque Metals Ltd (ASX: TOR)

- Greatland Resources Limited (ASX:GGP / AIM:GGP)

- Patterns

- Fundamental notes

- Crypto Bookmarks & Fees

- Risks & Mitigation

- Watch lists

- Metrics to enter

- Sunday scan checklist

- Stonk Links

- Long term ideas

- Tips & Useful Info

TA Notes

Pivot points, market structure & the three phases of major trends

Dow Theory — Foundation

Charles Dow is the grandfather of technical analysis. He co-founded the Dow Jones Industrial Average (1896, still running today) and the Wall Street Journal. His work was done without computers — all manually charted with pencil and paper.

The other three TA Titans built on Dow's work:

- Ralph Elliott — developed Elliott Wave Theory (wave structures driven by collective investor psychology). Dove deeper into the patterns within Dow's phases

- Richard Wyckoff — developed the Wyckoff Method, going deeper into exactly what accumulation and distribution phases look like (signature patterns)

- W.D. Gann — theories on price, time, and geometry. Everything runs on time cycles (life, weather, seasons — financial markets are no different)

The 6 Tenets of Dow Theory

Each tenet is covered in depth throughout the course. Summary:

- The averages discount everything — all available information (economic, political, market) is already reflected in price. "Buy the rumour, sell the news" — if you're hearing about it, professionals already knew

- The market has three trends — Primary (long-term), Secondary (medium-term), Minor (short-term). A common mistake: wanting to invest long-term but taking entries on minor short-term moves

- Primary trends have three phases — Accumulation, Public Participation, Excess/Distribution (this week's focus)

- A trend persists until its reversal is indicated — like Newton's first law: a trend stays in motion until acted upon. There are only three ways a trend can reverse (covered in Week 3)

- The averages must confirm one another — a trend needs confirmation from multiple sources, just like you'd research a major purchase from multiple angles, not just one data point

- Volume must confirm the trend — volume should rise with the trend. Big money can mask price action but they can't mask volume — you can't hide how many units were bought or sold

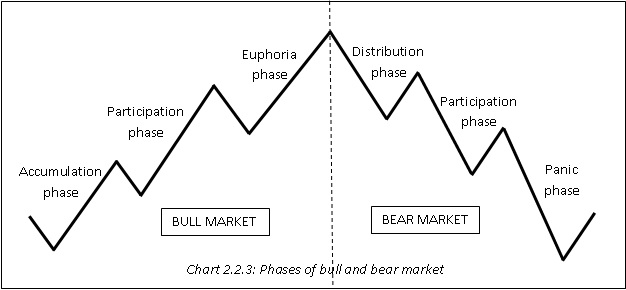

The Three Phases of a Primary Trend

A bull market is broken into three phases: Accumulation → Public Participation → Excess. Then it reverses through: Distribution → Public selling → Panic. Then it resets.

Phase 1: Accumulation

- Occurs after a prolonged decline or bear market

- Smart money / experienced investors start buying undervalued assets (just because something is down bad, doesn't mean it can't go down more)

- Market sentiment is very pessimistic — "this thing sucks", everyone expects it to keep going down

- Low trading volumes and gradual price stabilisation

- Key insight: "If everyone's bearish, who's left to sell?" — that's often where it finds a bottom

- Can last years (Microsoft went sideways for 14 years after the tech bubble, FMG went sideways for 10 years after the GFC)

The Spring / Liquidity Grab: During accumulation, big money often pushes price below the bottom of the range before sending it up. Why? Anyone who bought support had stop losses just underneath — big money grabs that liquidity, shakes people out, then sends it. If something breaks out of a major sideways range to the downside and pops straight back in — that's actually a sign of strength (a "spring"). The opposite applies to distribution: a pop above the range that falls back in is a sign of weakness.

Phase 2: Public Participation

- Momentum builds as more investors recognise the trend

- Media and public interest increases — some positive news articles, battle between bulls and bears

- Price rises significantly due to higher demand

- This is usually the longest phase — where the most gains come from

- Increased trading volumes

- Positive market sentiment, with a taste of euphoria toward the very end

- The really savvy investors get in early in this phase, majority get in mid-to-late

Phase 3: Excess

- Smart money begins selling at higher prices

- Can manifest as a blow-off top (fast spike then fast sell-off) or a long sideways distribution

- Overvaluation concerns arise but people start ignoring them ("maybe the market just likes it at this price")

- Sentiment is overly optimistic or euphoric — you'll struggle to find anyone saying anything bad about it. 90% bullish

- Declining trading volumes despite higher prices — price going up but volume not confirming (Tenet 6)

- Signs of reversal or instability may appear but average investors won't recognise them

The Sentiment Cycle

The emotional progression through the phases:

Bull market (going up): Disdain → Skepticism ("just a dead cat bounce") → Caution → Growing confidence → Conviction → Peak Greed/Euphoria

Bear market (coming down): Hope ("just another zig-zag") → Worry → Fear ("what have I done") → Disgust → Disdain

Peak fear at the bottom. Peak greed at the top. Every time.

Corrections Between Phases (Craig's Key Rule)

- After accumulation ends → expect a 1/3 to 2/3 pullback of the accumulation gains

- After public participation ends → expect a 1/3 to 2/3 pullback of the public participation gains

- After excess ends → you don't just correct the excess. You correct the ENTIRE move from the start of accumulation to the top of excess. These are the major resets (GFC wiped 57% off S&P, crypto cycles pull back 80%)

This is why getting caught buying in the excess phase is so dangerous — you're not just giving back the excess gains, you're giving back everything. It can take 6-13 years to recover.

Phases Within Phases (Fractal Nature)

Each major phase contains its own sub-phases of accumulation, public participation, and excess. The more you zoom in, the more sub-phases you see. This concept is the foundation of Elliott Wave Theory (Term 3).

Example: The S&P 500 since 2009 has a big accumulation, big public participation, and big excess phase. But within the big public participation, there were smaller accumulation, public, and excess sub-phases.

Commodity vs Equity Phase Differences

- Equities/Indices: Public participation is the dominant, longest phase. Accumulation and excess are often similar sizes

- Commodities (and commodity stocks like lithium, gold, uranium miners): The excess phase can be disproportionately massive — huge blow-off tops. Public participation can be relatively smaller

Examples

- Bitcoin 2018–2021: Sideways accumulation 2018-2020, public participation started when 20K broke (savvy ones got in at 12K), excess phase when everyone was talking about "who's buying next after Tesla" — they distributed into the good news

- Microsoft: Parabolic into 2000 tech bubble, crashed, went sideways for 14 years (accumulation), broke out ~$37 resistance, then public participation trending up

- FMG: Massive spike pre-GFC, crashed to $1, accumulated for 10 years at $1-7, broke out and ran to $23+

- Core Lithium: Went up 9,700% — but most holders didn't get out and gave it all back (lost 96% from top). Perfect example of why understanding excess phase matters

Pivot Points

If you cannot identify pivot points, you cannot identify market structure. If you cannot identify market structure, you cannot identify a trend. This is the literal backbone of technical analysis.

How to Identify Pivot Points

- Look for 3 candles moving in the opposite direction — this is not a textbook rule, it's a beginner-friendly method to stop you getting faked out on tiny moves. ~90-95% of pivot points will follow this rule

- They don't have to be 3 red or 3 green candles — they can be a mix of colours. You're looking for the overall direction changing (3 candles moving the opposite way to the primary move)

- Exceptions: During elevated market volatility, 1-2 very large candles can count as a pivot (e.g. a big bullish engulfing candle on its own)

- Craig's clarification: The 3-candle rule is a guide to prevent you marking 100 tiny pivots that add no value. What you're really looking for is significant peaks and significant troughs. If it's just undulating noise, you probably don't need a pivot there

Pivot Point Shapes

- V-shaped: Rapid, sharp reversal — price quickly changes direction. Most common

- U-shaped: Gradual shift — price hangs around the bottom/top sideways for a bit before reversing

Swing Highs and Swing Lows

Pivot points are also called swing points:

- Swing High (H): Pivot at the top where sellers step in — identifies resistance levels

- Swing Low (L): Pivot at the bottom where buyers step in — identifies support levels

Practical Tips for Marking Pivots

- Use the highlighter tool in TradingView (small dots) to mark pivots

- Colour code: green dots for lows/buyers, red dots for highs/sellers — green=go, red=stop

- Line chart trick: Switch from candles to line chart to more easily see pivots when the wicks and candles are clouding your judgment. It strips away the noise and shows the pivots clearly

- Hold Ctrl + click on a dot to drag-copy it (saves time vs recreating each one)

- Start on the weekly timeframe — Dow himself never traded below the daily because it was all manipulated noise. The lower you go, the harder it gets. Weekly for the first 6 weeks minimum

The 3 Types of Market Structure

There are only 3 things a market can do: go up, go down, or go sideways. The first thing you should do when pulling up any chart is identify pivot points, then identify market structure.

"Market structure is king" — when you go against market structure, that's when you lose.

Bullish (HH / HL)

- The market is going up

- Marked by consistent higher highs and higher lows

- Pivot peaks are higher than the previous highs — signals increased demand and optimism (sellers selling higher each time)

- Pivot lows are higher than previous low — signals resilience, buyers stepping in higher each time (buyers believe it won't go back to the old price)

- Think: "Why are they buying at $18K when last time they didn't buy until $16K? Why are they selling at $20K when last time they sold at $18K?" — that's a strong uptrend

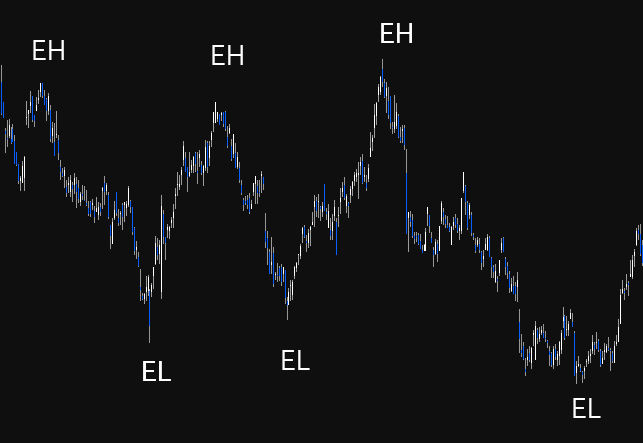

Consolidation (EH / EL)

- Market moving sideways

- No clear trend — equal highs (selling at roughly the same level) and equal lows (buying at roughly the same level)

- Traders look for breakouts (above EH = potential uptrend) or breakdowns (below EL = potential downtrend)

Bearish (LL / LH)

- The market is going down

- Lower Lows: each trough is lower than the previous — buyers waiting for lower prices each time

- Lower Highs: each peak is lower than the previous — sellers stepping in earlier each time, don't believe it will reach the previous high

- Think: "Why are they selling at $22K when last time they were selling at $23K? Why are they buying at $19K when last time they bought at $21K?"

- Can be good for shorting

Market Structure Change Confirmation

You need BOTH to confirm a change:

- Bullish change: need a higher high AND a higher low. Getting just a higher high with a lower low is NOT a change — buyers are still coming in lower (still bearish)

- Bearish change: need a lower low AND a lower high. Getting just a lower low without a lower high is NOT confirmed

Connecting Pivots

Draw a line connecting your pivot points to visually see the trend direction. This makes it obvious when you transition from uptrend → sideways → downtrend.

Transition Through Phases Using Market Structure

Markets transition: Uptrend (HH/HL) → Sideways (EH/EL) → Downtrend (LL/LH) and vice versa. The phases map directly: Accumulation = sideways (EH/EL), Public Participation = uptrend (HH/HL), Excess = potentially still making highs but with warning signs, Distribution = begins transition to LL/LH.

Supply & Demand, and Support & Resistance

Dow Theory Tenet 2: The Market Has Three Trends

The market moves in three distinct types of trend, each operating on a different timeframe. Understanding which trend you're looking at is critical — your timeframe must match your investment/trading goals.

Primary Trend (The Tide)

- The most significant and long-term trend — lasts months to years

- Most reliable for investment decisions because it's less prone to manipulation

- Two types: bull market (upward) and bear market (downward)

- Like the tides of the ocean — shows the long-term direction

- The primary trend cannot be stopped by any macro event. Wars, depressions, pandemics, financial crises — on the S&P 500's 100-year chart, they're all just blips on a trend that keeps going up

- If you're investing long-term (years), you should be looking at the 3-monthly (quarterly) timeframe or above

Secondary Trend (The Waves)

- Temporary movement in the opposite direction to the primary trend

- Lasts several weeks to several months (the example shown was ~7-8 months)

- Retraces approximately 1/3 to 2/3 (or half to two-thirds) of the primary trend's movement

- The "zag" in the zig-zag — if the primary trend is the zig (direction), the secondary trend is the zag (correction)

- Two types of corrections: sharp (fast V-shaped drops) or sideways (extended horizontal movements). Both are secondary corrections

- Key rule: The primary trend resumes when price surpasses the highest/lowest point of the secondary action. If it can't get back above that point and breaks the secondary low on increasing volume, it may signal a new primary bear trend rather than just a correction

- The 50% retracement level is emphasised by Dow Theory as particularly significant

Minor Trend (The Ripples)

- The shortest trend — lasts days to weeks

- Daily market fluctuations — compared to ripples on waves (can't predict which way they'll go)

- Erratic, can be manipulated, and is largely noise

- The only thing worth paying attention to within minor trends are horizontal lines on daily charts (support and resistance) — which is what this week covers

- Dow considered everything below the daily to be manipulated noise

How They Interact

The zig is the primary trend direction. The zag is the secondary correction. Within both, the minor trend creates the day-to-day ripples. When investing, you care about the primary. When trading, you're navigating the secondary and minor within the context of the primary.

Support & Resistance — Psychology

Support and resistance are fundamental concepts tied to the principles of supply and demand. They represent the battlegrounds where supply and demand forces collide.

Psychological Impact

| Support | Resistance |

|---|---|

| Price points where buyers typically step in, perceiving the asset as undervalued | Psychological barriers where sellers see the asset as overvalued |

| Traders associate these levels with safety nets, triggering buying pressure | Leads to increased selling pressure — hesitation, shorting, or profit-taking |

Breakouts and Failures

When support or resistance levels are breached, they signal shifts in sentiment — either stronger conviction (breakout) or panic selling (breakdown), leading to rapid price changes. Recognising these psychological shifts helps anticipate market moves.

Supply & Demand

Financial markets work exactly the same as any marketplace — it's all supply and demand. Think of it like a flea market, or bartering in Bali. Prices move based on the balance between willing buyers and willing sellers.

Key principle: For every buyer, there is a seller. For every seller, there is a buyer. It doesn't just magically go somewhere — when you're selling, someone else is buying because they think it's a good deal.

Demand Zones

- Areas where a large volume of buy orders accumulate

- Signal strong belief in potential price increases

- When price reaches a demand zone, it tends to stop falling because there are many buyers looking to purchase

- Think: only 2 Ferraris for sale at $100K but 100 people wanting to buy — bidding war pushes price up

Supply Zones

- Areas with concentrated sell orders

- Traders expect prices to decline due to perceived overvaluation

- When price reaches a supply zone, it may stop going up because there are too many sellers trying to get rid of their stuff

- Think: thousands of people trying to sell Ferraris at $100K — too many options, price can't go higher

Everything Has a Price

Even the worst-performing assets eventually reach a price where someone thinks it's cheap and demand steps in. Examples:

- AGL: From $28 down to $5 — "it's a dog, it's the worst" — but demand stepped in at $5 and it recovered to ~$12

- ZIP: From $14 down to ~$0.20 — at some point buyers perceived value, it bounced to ~$3

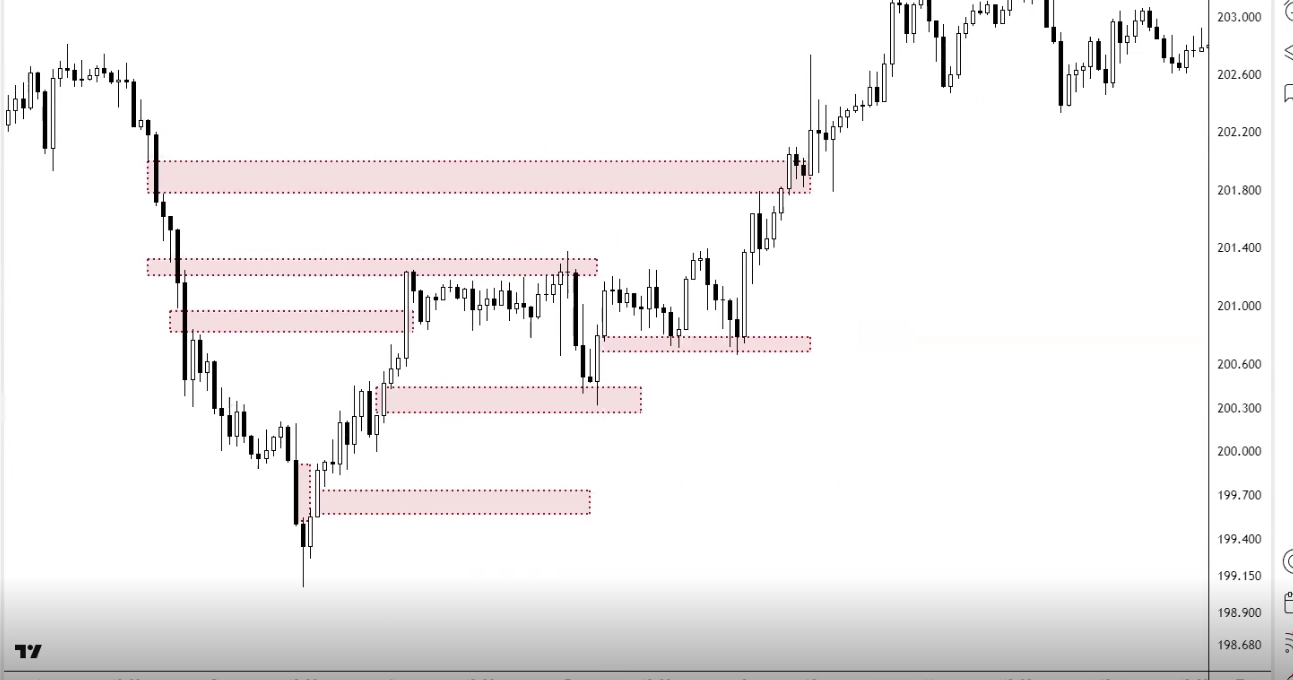

Support (Demand)

Support is a price level where an asset usually stops falling and starts to see more buying. It marks a point where the balance between supply and demand shifts in favour of demand.

Key Concept: Support is a ZONE, Not a Line

Never draw support as a single line — it doesn't work. Support is always a zone (a range) where historical buying interest has caused price reversals. Buyers don't step in at one exact price — they step in around an area.

Example: Buyers might step in at $208, $209, $212, $214, $211 — that's all a zone around $208-$214, not a precise price point.

Visualising Support

Think of it literally as people standing at different price levels willing to buy:

- $38: one person → weak support

- $33-$34: two people → bit of a demand zone

- $30: one more person → some support

- If $30 breaks, nobody until $24-$25 → price will fall quickly to the next cluster of buyers

- Below that, nobody until $9-$10 → another rapid drop

The gaps between clusters of buyers are where price moves fast — when support breaks, it falls to the next level where people are willing to buy.

How to Draw Support Zones

- Find your pivot points where buyers have stepped in (swing lows)

- Look for multiple pivot lows clustered around a similar horizontal area (like "dot to dot")

- Use the rectangle tool in TradingView (5th icon down → click arrow → Rectangle)

- Draw the rectangle encompassing as many of those candlestick wicks as possible

- Change the colour to green (Settings → Border → green, Background → green, lower transparency so candles are still visible)

- Add text label "Support" for quick identification

Support Key Points

- Analyse support on multiple timeframes — daily, weekly, monthly. Higher timeframe support is more reliable (monthly > weekly > daily > 4H > 1H)

- Identify major support — strong levels that have held over a long period and are respected by many traders

- Use support levels for determining entry points and setting stop losses

- If price breaks through support, it can trigger sell-offs as traders' stop losses get hit — price then falls to the next support zone

Resistance (Supply)

Resistance is a price level where an asset tends to stop rising due to selling pressure. It represents areas of supply where sellers are willing to exit.

Key Concept: Resistance is Also a ZONE

Same as support — resistance is always a zone, not a single line. Sellers step in around an area, not at one exact price.

Example: Sellers might step in at $228, $230, $232, $234 — that's all a zone around $230, not a precise price.

How to Draw Resistance Zones

- Find your pivot points where sellers have stepped in (swing highs)

- Look for multiple pivot highs clustered around a similar horizontal area

- Use the rectangle tool, encompassing as many candlestick highs/wicks as possible

- Change colour to red (Border → red, Background → red, lower transparency)

- Add text label "Resistance"

The Battle Between Bulls and Bears

Once you have support (green) and resistance (red) drawn, you can see the battle. Eventually one side wins:

- Sellers get exhausted → bulls win → breakout upward

- Buyers get exhausted → bears win → breakdown downward

Resistance/Support Flip (Role Reversal)

"If you can master this strategy, you can honestly make money on the market." — ASX Trader

A resistance/support flip occurs when a former resistance level becomes a new support level (or vice versa). This is one of the most powerful concepts in technical analysis.

How It Works

- Price approaches resistance repeatedly — sellers step in each time

- Eventually, sellers get exhausted — no more sellers left at that price

- Price breaks through resistance (breakout)

- Price comes back to test that old resistance level

- Those sellers have now become buyers — old resistance is now support

- The flip is confirmed

What It Signals (Two Buy Signals)

- Sellers are exhausted — they're no longer stepping in at that price

- Sellers have become buyers — the level that was previously seen as overvalued is now seen as undervalued

The Fake-Out Warning

If price breaks out of resistance but immediately pops back within the zone, that's a sign of weakness (fake-out), not a genuine breakout. The opposite also applies — breaking below support and popping straight back in is a sign of strength (this links to the "spring" concept from Week 1).

CBA Example — The Staircase

Commonwealth Bank's entire existence is essentially a series of resistance/support flips — climbing steps:

- $7 resistance → became support → $9.90 resistance → became support → and so on

- Tech bubble bottom support at $23-$25 zone → held during GFC (buyers stepped in at the same zone again across 10+ years)

- GFC top resistance at $60 → exhausted → broke through → during COVID drop, $60 became support (people saw it as cheap at $60 when they previously thought it was overvalued)

- As long as it keeps climbing steps (flipping resistance to support), it's in an uptrend. If it starts breaking below support floors, each floor becomes the next ceiling on the way down

Trading Strategies Using Support & Resistance

1. Breakout Strategy

Objective: Profit from significant price movements following a breakout of support or resistance.

- Buy when price breaks above resistance (sellers exhausted)

- Sell/short when price breaks below support (buyers exhausted)

- Stop loss: Just below the pivot low (for longs) or just above the pivot high (for shorts)

2. Pullback/Retest Strategy (Resistance/Support Flip)

Objective: Enter trades when price retraces to a support/resistance level after a breakout.

- Wait for breakout through resistance

- Wait for price to pull back and test old resistance as new support (the flip)

- Enter when it bounces off the new support

- This is probably the best strategy — it gives the ultimate risk:reward because you get two confirmations: (1) sellers exhausted, (2) sellers become buyers

- Stop loss below the new support zone

3. Range Trading Strategy

Objective: Profit from price fluctuations within a defined sideways range.

- Buy at support, sell at resistance — repeat until the range breaks

- When it breaks out → switch to breakout or pullback strategy

- ASX Trader's view: "I personally don't touch sideways markets." He only trades trending markets (bull or bear). Range trading can get messy — price doesn't always bounce cleanly off the boundaries

- Key insight: People don't lose money in bull or bear markets — they lose money in sideways markets. They keep trying to go long or short, keep getting stopped out, and lose trade after trade

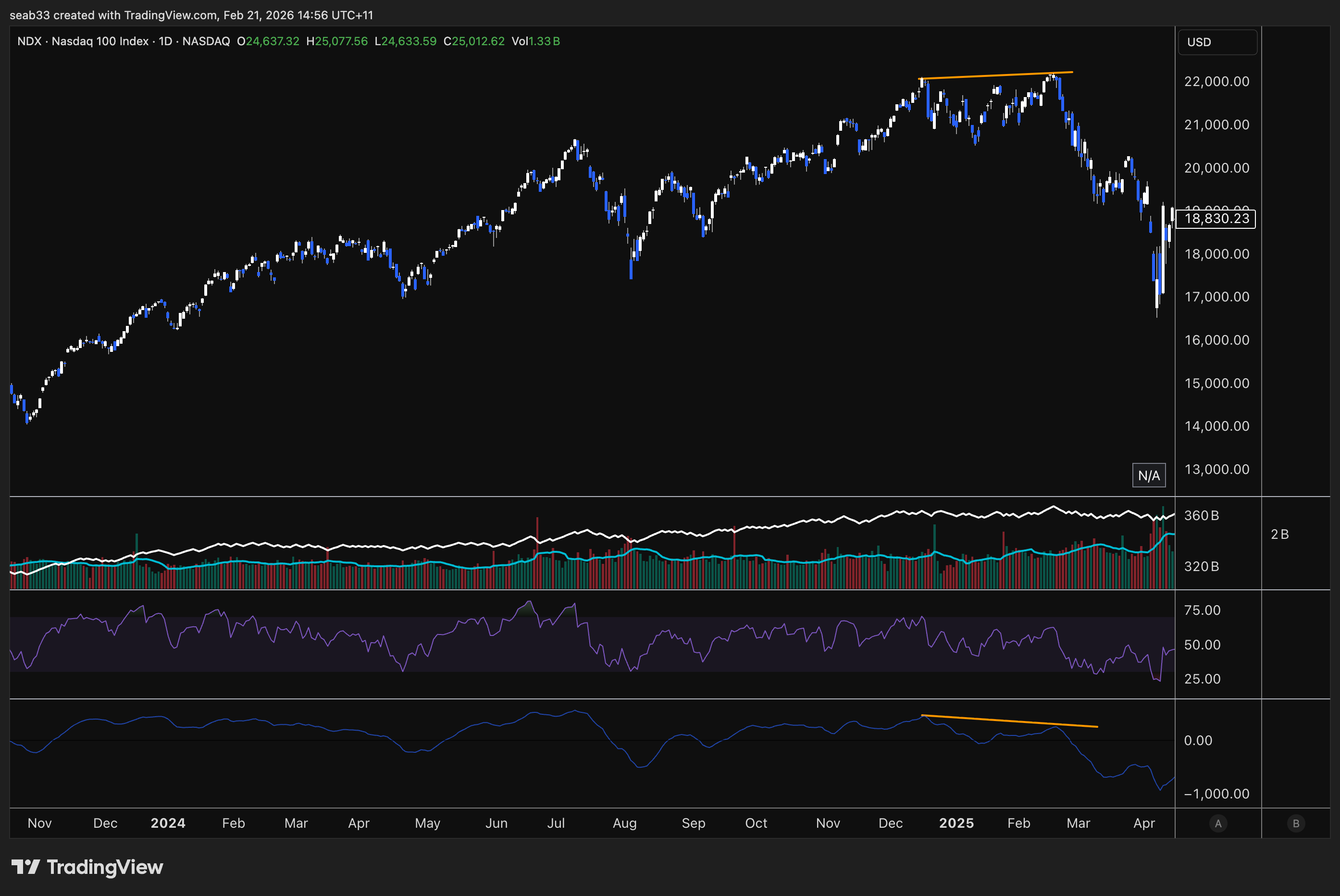

1.3 - Reversal patterns, trend lines & channels

Dow Theory Tenet 4: The Trend Is Your Friend

A trend will persist until its reversal is indicated. Like Newton's first law — an object in motion stays in motion unless acted upon by an external force. A market trend stays in motion until external factors cause a shift (fundamental news, economic data, or exhaustion in buying/selling pressure).

Why Trend Recognition Matters

- Prevents emotional trading — instead of guessing tops and bottoms, follow the existing trend

- Improves risk management — place stop losses under pivot lows, falling with market structure

- Maximises profit potential — trading in the direction of the trend increases probability of success

- Stay with the trend until price action (and later, volume) confirms a change

The Three Reversal Patterns

There are ONLY three ways a trend can reverse. Every reversal pattern you'll ever see fits under one of these three. That "cheat sheet with 50 different reversal patterns"? They're all just versions of these three.

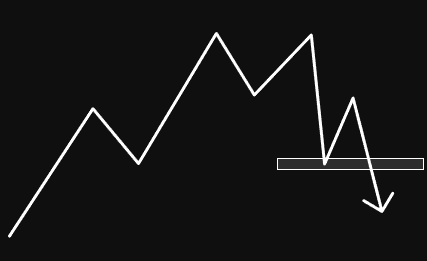

1. Double Top / Double Bottom

The most common reversal pattern. Often called the "M pattern" (tops) or "W pattern" (bottoms). You can make money literally just trading these — they're textbook and easy to identify.

Double Top formation:

- Price reaches a peak (point 1), retraces to a low (point 2)

- Rallies back up but fails to exceed the previous high — selling equal (point 3). First warning sign: "Why are they selling at the same price? Every previous time they sold higher"

- Declines and breaks below the support at point 2 (the "neckline"). First sell signal: sellers won. Buyers who stepped in at point 2 are no longer there

- Often retests the neckline as resistance (support/resistance flip) — because anyone who bought the dips now wants out if it gets back to their buy price

- Confirmation: when price breaks point 6 (below the retest low) = lower low, lower high, lower low = change of market structure

The psychology:

- Point 1 & 3: "I should have sold at $11. If it ever gets back there, I'll sell next time." The market gives second and third chances — it's uncanny how often this happens

- Point 2 vs 4: "They were willing to buy at $7.80 last time (point 2). Now they're not buying there. Where did those buyers disappear to?"

- The neckline break is pivotal: sellers at the same spot + buyers NOT at the same spot = bears won

Measured target: Distance from the double top to the neckline, projected downward from the neckline breakout point. That's your approximate target for the move.

Negation: If price gets back above the neckline, the double top is over — no longer expecting lower moves.

Double Bottom is the exact opposite. W-shaped. When you get big double bottoms over a large timeframe, they're textbook accumulation zones. Examples: FMG post-GFC ($1 double bottom), Apple ($13 double bottom), Cardano ($0.02 double bottom), Ethereum 2018-2020 double bottom.

For confirmation purposes, treat a double bottom exactly like a failure swing — the high between the two lows is the neckline, and confirmation is when you close above it.

2. Non-Failure Swing (STRONGEST Reversal)

The most powerful reversal because you're not only breaking prior pivots but also getting a confirmed lower low, lower high, lower low (change of market structure).

Non-failure swing top:

- HH, HL, HH, HL pattern — uptrend proceeding normally

- Price makes a new high (point 5) — still going higher, all good

- Then drops below the previous higher low (point 4) — penetrates prior pivot. First warning sign

- This is where "buy the dip" gets dangerous — people keep buying the dip because it worked every other time. But when you can read market structure, you realise this is NOT the time to buy the dip. This is when big money distributes INTO the dip

- Rally back up but now forming a lower high (point 7) — second warning sign. "Why are they selling at $59K when every other time they sold at $64K, $61K?"

- Breaks below the prior low — confirmation. "This should be an absolute bargain. Why aren't they buying again?"

Two sell signals:

- Sell signal 1: When it breaks below the prior pivot (the first lower low)

- Sell signal 2 (stronger): When you get lower low + lower high + lower low = confirmed change of market structure

Why it's the strongest: Unlike the failure swing, a non-failure swing breaks through prior pivots AND gives you the full LL/LH/LL confirmation. The psychology flip is complete — people who were "buying the dip" every time are now watching it power straight through their buy levels.

Example: Bitcoin at $64K top and $30K bottom were both non-failure swings.

3. Failure Swing (LEAST Reliable)

How to identify (in a downtrend): The first sign is it fails to make a new low. Instead of continuing lower, it puts in a higher low. Then takes out the previous high.

How to identify (in an uptrend): The first sign is it fails to make a new high. Price makes a lower high, then breaks below the previous low.

Why it's called "failure" swing: Because the dominant trend failed to continue — it failed to make a new low (in a downtrend) or new high (in an uptrend).

Why it's the least reliable: It can just be an ABC correction (3 steps forward, 2 steps back). The market might bottom shortly after the failure swing exit and then continue the original trend. More depth on this comes with Fibonacci and zig-zag zones later in the course.

A head & shoulders pattern is just a version of a failure swing. Shoulder, head, other shoulder — it's the same structure.

Craig's Key Confirmation Rules (Apply to ALL Three)

The critical thing that's the same across all three reversal patterns:

- Regardless of whether the higher high or higher low comes first, you must close above the previous high (in a downtrend reversal) to get confirmation

- Use candle BODY closes, not wicks. Draw the confirmation line on the candle body. You need a candle close above that level, not just a wick

- Match your timeframe: Weekly close for swing trades (most reliable, sets you up for months). Daily close for shorter trades (changes structure every few weeks). Hourly for intraday (lasts only hours)

- Weekly confirms are much more reliable than daily. A weekly change of market structure holds for a long period. Daily can flip back and forth quickly

- Once market structure has changed, you DON'T need to wait for reversal confirmation again on pullbacks. After confirmation (bearish → bullish), pullbacks in a bullish structure are buying opportunities. You only need the full reversal confirmation once — when the trend actually changes direction

The Non-Failure vs Failure Naming (Craig's Simple Explanation)

In a downtrend:

- Failure swing: The first sign is it failed to make a new low. Then it takes out the high → confirmation

- Non-failure swing: It did NOT fail to make a new low first. Instead, the first sign is it took out the previous high. Then it makes a higher low. Then confirms by taking out the next high → confirmation

In both cases, the final confirmation step is the same: close above the previous high.

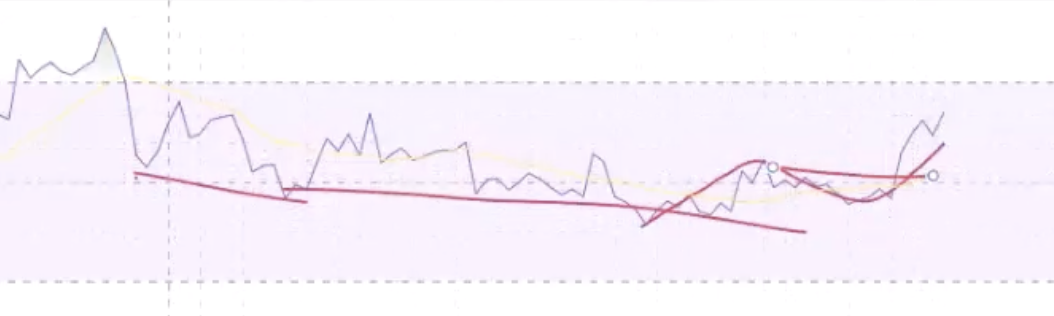

Trend Lines

Trend lines use the same concepts as horizontal support/resistance (above = resistance, below = support) but at an angle.

How to Draw a Bullish Trend Line

- Find the lowest point of the price

- Find the next 1-2 higher lows and connect a line across those points

- Draw the trend line below the price (it acts as support — the floor)

- Can include a mix of candle bodies or wicks — context is key

- Two points to draw, three points to confirm. The third touch validates the trend

How to Draw a Bearish Trend Line

- Find the highest point of the price

- Find the next 1-2 lower highs and connect a line across those points

- Draw the trend line above the price (it acts as resistance — the ceiling)

- Try to encompass as many touches as possible — the more data confirming the line, the stronger it is

Key Principles

Dow Theory states that the only valid trend lines are horizontal — because angled trend lines are subjective (open to interpretation depending on how you draw them). You can draw two completely different trend lines on the same chart and both could be "right."

Don't get caught up on exactly how the trend line is drawn. They're a signal, not gospel. What you're looking for is when the trend may be about to change. The confirmation is always the change of market structure (HH/HL or LL/LH), not the trend line break itself.

Trend line breakout + retest as support = same concept as horizontal S/R flips. Very common for broken trend lines to get retested.

Advanced Trend Lines

Acceleration & Deceleration (Angular Momentum):

- Upside acceleration = bullish, but if rate of ascent is excessive, it may not be self-sustaining (blow-off top / buying climax that collapses)

- Upside deceleration = bearish (candle ranges getting smaller and smaller — buying momentum fading)

- Downside acceleration = bearish, but may end in a selling climax

- Downside deceleration = bullish

Measured Target for Trend Line Breakouts: Take the maximum distance price has moved away from the trend line, and project that same distance from the breakout point. That's your minimum price target.

Hot tip: The easier it is and the more people that can spot the trend, the closer you are to it ending. When every man and his dog can see it, it probably won't hold.

Channels

A channel is a set of parallel trend lines (like train tracks) defined by the highs and lows of price action. They present great trading opportunities and help with risk management.

Three Types

- Ascending (bullish): Parallel upward lines — HH/HL. Buy at support (bottom line), sell at resistance (top line)

- Descending (bearish): Parallel downward lines — LL/LH. Short at resistance (top line), cover at support (bottom line)

- Sideways (neutral): Horizontal parallel lines — EH/EL. Buy at support, sell at resistance until breakout

How to Draw Channels

- In TradingView: left toolbar → Trend line → arrow → Parallel Channel

- Find the lowest point (for ascending) or highest point (for descending)

- Draw along the support touches, then drag up/down to encompass resistance touches

- Try to get as many touches on both lines as possible

The Midline

The dotted midline of a channel often acts as its own support/resistance level. Price frequently bounces off or rejects from the midline — the "return to mean."

Channel Validity

- Valid as long as price touches support at least twice and resistance at least three times (or vice versa)

- Breakout below support in an ascending channel signals potential reversal

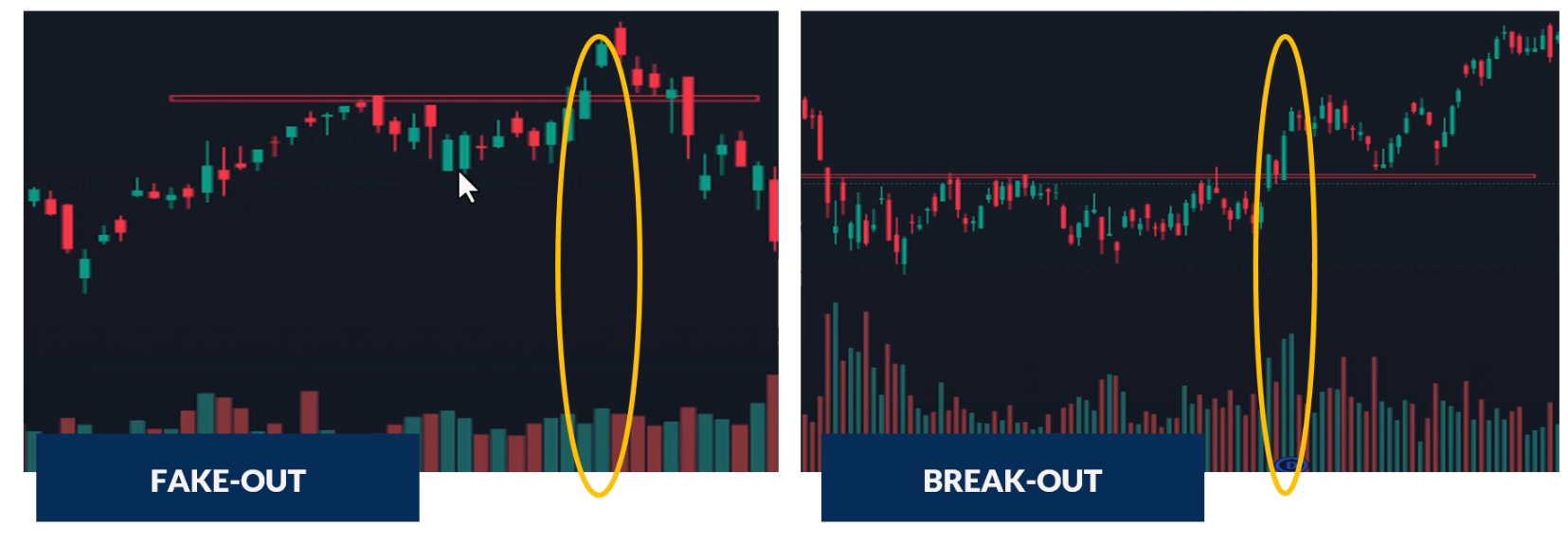

- Breakout vs fake-out: If it breaks out and comes straight back in, it's probably a liquidity grab. If it breaks out and continues, it's a genuine breakout

Channel Exhaustion

If price fails to reach the upper line of an ascending channel, that's an early warning of trend exhaustion. The breach of the lower support line becomes more likely after a failure to reach the top.

S&P 500 100-Year Channel Example

Drawing a channel from the top of the Great Depression through the tech bubble on a 3-monthly chart shows that historically, when the S&P hits the upper channel resistance, it corrects back to at least the midline (dotted line). If things get really bad and oversold, it can come all the way back to the bottom channel line. This gives context for when things are at resistance, around the mean, or extremely undervalued.

1.4 - Volume analysis, Wyckoff techniques & On-balance Volume

Dow Theory Tenet 6: Volume Must Confirm the Trend

Volume is just the total number of shares/coins that changed hands in a period. Nothing more. It has nothing to do with price directly — it's simply how many units were traded. Think of volume as the fuel for the market — running on low fuel, it won't go far. Full tank, it'll keep going.

If volume is increasing along with the price trend, it suggests smart money is buying into the trend. Smart money owns billions and generates the majority of volume. If volume doesn't confirm the move, it's likely dumb money (untrained retail traders) moving the price.

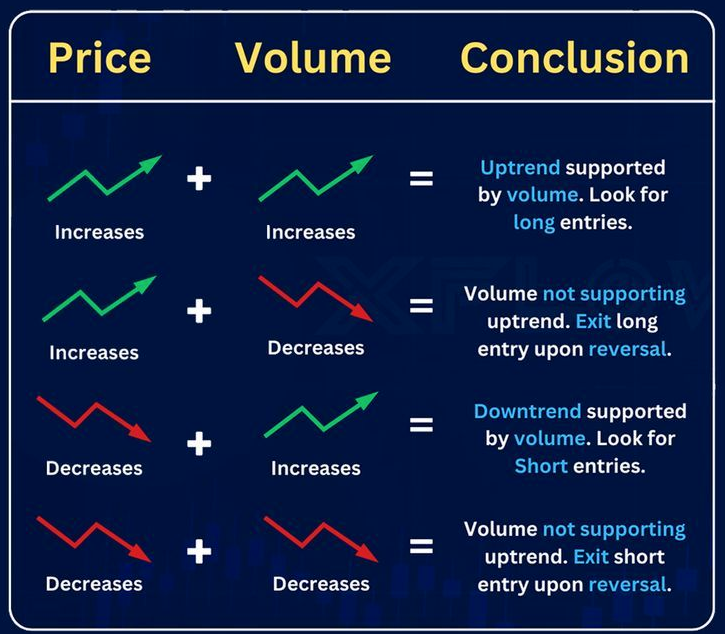

The Four Price-Volume Relationships

| Price | Volume | Signal | Meaning |

|---|---|---|---|

| Rising ↑ | Rising ↑ | Bullish — good for longs | Uptrend supported by volume. Stay in longs |

| Rising ↑ | Falling ↓ | Bearish — look to exit | Uptrend NOT supported by volume. Look to exit on further signs of reversal |

| Falling ↓ | Rising ↑ | Bearish — good for shorts | Downtrend supported by volume. Exit longs or look for shorts |

| Falling ↓ | Falling ↓ | Bullish — likely a pullback | Downtrend NOT supported. Probably just a correction/zag, not a new trend |

The biggest misconception: People think rising volume = good, falling volume = bad. Wrong. Rising volume just means the current trend is supported. If the trend is DOWN and volume is rising, that's confirming the downtrend — lots of people are still selling.

Key connection to Dow Theory: The secondary action (1/3-2/3 retracement) should happen on decreasing volume because it's a corrective move, not a new trend. Volume should support the primary trend, not the secondary correction.

Volume at Breakouts: Fake Out vs Breakout

- High volume on breakout = genuine breakout. Volume confirms the move. Smart money is behind it

- Low or declining volume on breakout = likely fake out. Lack of interest, higher probability of false breakout

- Now whenever you see a change of market structure or break of S/R, check volume to confirm it's probably real

Volume at Support & Resistance

When there's high trading activity at support/resistance levels, those levels are more reliable — lots of investors treating them as buy/sell points means they'll likely continue to do so. High volume at support = probably going to hold. High volume at resistance = probably going to reject.

High Volume Spikes

High volume spikes tend to happen at extreme tops and extreme bottoms — that's where the most buyers and sellers are active:

- At bottoms: Capitulation — hesitant investors finally give up and massively sell. Volume spike marks the exhaustion of selling

- At tops: Exhaustion moves — climactic buying followed by sharp reversals

Wyckoff's Third Law: Effort vs Result

Richard Wyckoff (1873-1934), one of the TA Titans, developed a key principle about the relationship between volume (effort) and price movement (result).

Price-Volume Convergence (Effort = Result)

When both price and volume move in the same direction, market participants are in agreement. Large body candles + large volume = convergence. The current trend is likely to continue.

Gym analogy: If you go to the gym every day for 3 months (big effort), you should see your body change (big result). That's convergence — effort matches result.

Price-Volume Divergence (Effort ≠ Result)

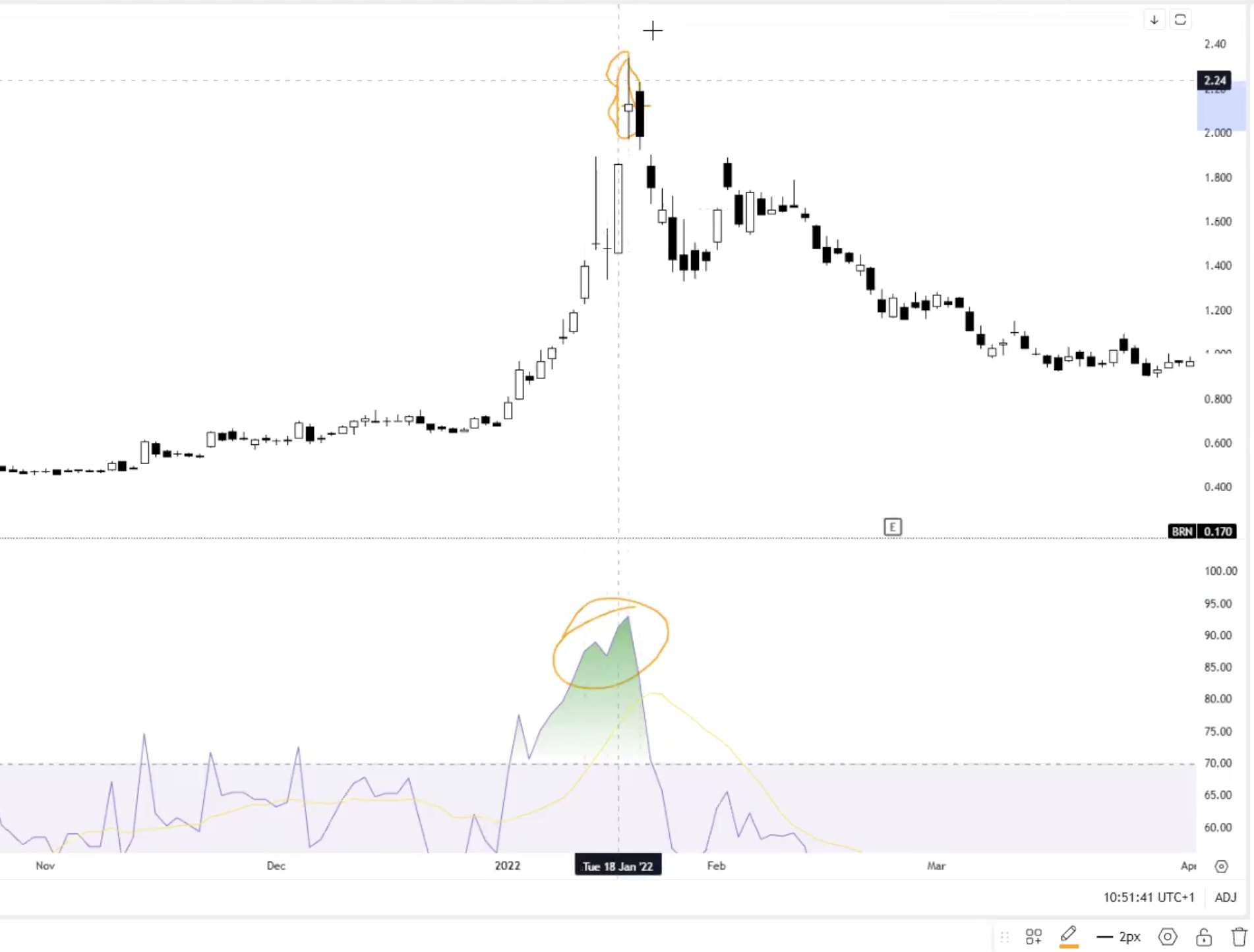

Small candle body + high volume = potential shift in market sentiment. The market required a lot of effort but barely moved — something is wrong. High volume doji candles are classic divergence signals and often precede reversals.

Gym analogy: If you go to the gym every day for 3 months (big effort) and look in the mirror and nothing's changed (no result) — something's up.

On-Balance Volume (OBV)

Created by Joseph Granville in 1963. His theory: changes in volume precede price movements. OBV is a leading indicator — it changes direction before price does.

How to Add OBV in TradingView

Indicators → search "OBV" → On Balance Volume → add. The blue line appears below the chart. Double-click anywhere blank on the chart to hide/show it quickly.

How OBV Works

OBV is a cumulative running total of volume — adding volume on up days, subtracting on down days:

- OBV line rising = volume on green candles is higher than volume on red candles = buying pressure = bullish

- OBV line falling = volume on red candles is higher than volume on green candles = selling pressure = bearish

- OBV line sideways = equal volume on up and down days = on par

The King & Queen Rule (CRITICAL)

"Price action is king. OBV is the queen. Listen to the king first, then see if the queen supports what the king is saying. Do NOT listen to the queen first."

Follow your price action first — market structure, reversal patterns, everything you've learned. Once you identify a setup, THEN check if OBV supports it. Do NOT look at OBV first and try to make the price action fit. You will get wrecked doing it backwards.

Detox your charts: Remove all indicators. Analyse price action clean. Only then add OBV to confirm. The price action is primary data, OBV is secondary.

The Five OBV Scenarios

1. Bullish Divergence Breakout: OBV reaches a new high while price approaches resistance → predicts price will break through resistance and head higher. OBV is leading — it's already broken out before price has.

2. Bearish Divergence Breakout: OBV hits a new low while price tests support → predicts price will break support and head lower. OBV already broke support before price did.

3. Bearish Divergence Reversal: Price rises to a new high while OBV hovers at or below the previous resistance level → predicts the rally will stall or reverse. Volume is NOT confirming the new highs. If price keeps making new highs but OBV keeps hitting a wall — that's bearish divergence.

4. Bullish Divergence Reversal: Price hits a new low while OBV stalls at or above the last support level → predicts the sell-off will stall or reverse. Price made a new low but volume didn't — something different, bullish divergence.

5. Convergence (Bullish or Bearish): OBV matches price action — when price goes up, OBV goes up; when price goes down, OBV goes down. This confirms the current trend is valid.

The Simple 95% Use Case

Most people (and this is perfectly valid) use OBV for one thing: does the OBV line do the same thing as price? When price makes HH/HL, does OBV also make HH/HL? If yes, volume confirms the move. If not, something's different. That alone is quite powerful as a confirmation tool.

Advanced OBV Strategies

Drawing TA on OBV

Everything you've learned from price action — support, resistance, trend lines, market structure — can be applied directly to the OBV line:

- Trend lines on OBV: Draw bullish/bearish trend lines on OBV just like on price. When OBV breaks its downtrend line, it can signal a reversal before price breaks its own trend line

- Support/resistance on OBV: Horizontal S/R zones work on OBV. When OBV breaks support that becomes resistance (same flip concept), it confirms the move

- Market structure on OBV: Look for HH/HL or LL/LH on the OBV line — it often changes structure before price does

OBV as Leading Indicator (Key Examples)

ASX Trader's Bitcoin call at $65K top: OBV broke its uptrend line while price was still making new highs. OBV had bearish divergence + trend break = exit signal. Price didn't actually break its trend until much lower (~$51K). OBV led the way.

Getting back in at the bottom: OBV broke its downtrend line and showed bullish divergence before price broke out. Combine downtrend break on OBV + bullish divergence = entry signal.

Avoiding Fake Rallies with OBV

When you see a rally and think it's a breakout — check if OBV has also broken its downtrend line. If OBV hasn't broken its decline, the rally is likely a fake. This stops you entering fake rallies. Match the actual breakout point on OBV (using a vertical line) with where price breaks out — they should align at the genuine breakout, not the fake ones.

Note: Fibonacci Clusters

The Fibonacci clusters lesson was included in this week's content but relates more to the Fibonacci & Retracement Zones topic. Key concept: overlay Fibonacci retracements from multiple timeframes (e.g. daily retracement + monthly retracement) to find "cluster zones" where multiple Fib levels overlap — these are stronger support/resistance zones than a single Fib level alone. Example: Microsoft's 618 from the COVID bottom overlapping with the 382 from the entire move created a powerful cluster support zone.

1.5 - RSI Divergence as a leading Indicator

What Is RSI?

The Relative Strength Index is a price momentum indicator — it measures price momentum only, nothing to do with volume. RSI is bounded between 0 and 100, like an elastic band that gets stretched between extremes and always snaps back.

Overbought & Oversold

- Above 70 = overbought. Above 80 = really overbought

- Below 30 = oversold. Below 20 = really oversold

- Between 30-70 = neutral

- RSI is considered "reset" when it moves from one extreme to the other (e.g. 70 down to 30)

Critical rule: Just because it's overbought doesn't mean it can't go higher. Just because it's oversold doesn't mean it can't go lower. Some of the BIGGEST moves happen when RSI is overbought or oversold. Don't sell just because it's overbought or buy just because it's oversold — that's using RSI as a lagging indicator and will get you wrecked.

RSI Reset Timing by Timeframe

- Hourly: Can reset from overbought to oversold within a single day

- Daily: Takes a few weeks of significant movement to reset

- Weekly: Can take several months (6+ months) to move from oversold to overbought

- A small pullback with a pivot is enough to reset RSI and allow the next leg up/down — the pullback doesn't have to be huge

How to Add RSI in TradingView

Indicators → search "RSI" → Relative Strength Index → add. Appears as a bounded chart below the price chart.

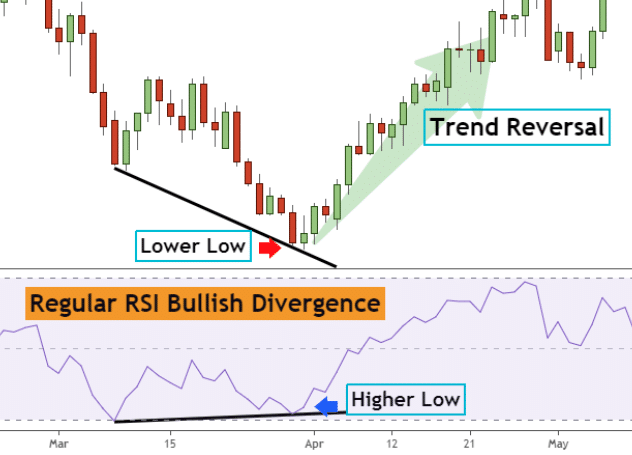

What Is Divergence?

Divergence is when price and the indicator (RSI) are going in opposite directions. It warns that the current price trend may be weakening and in some cases may lead to a reversal.

The running analogy: When you go for a run, at first you have all the energy and momentum. Over time, your body starts giving you signals — puffing, sweating, needing water — that you're weakening. Eventually you'll need to stop. The market works the same way. A trend is running strong, then RSI starts giving signals that momentum is fading. It doesn't mean the trend stops immediately, but it's warning you.

Using RSI for Divergence = Leading Indicator

If you use RSI for overbought/oversold, it's a lagging indicator (telling you what already happened). If you use RSI for divergence, it becomes a leading indicator — signalling what's likely to happen in the future. Every indicator the educator teaches is a leading indicator, because you can't make money on the past.

Divergence Can Mean Two Things

- Reversal — the trend actually reverses

- Range/Consolidation — price goes sideways to "chill" before continuing

Divergence does NOT always mean a reversal. It signals that something is changing, and the trend may consolidate OR reverse.

Two Types of Regular Divergence

| Bullish Divergence | Bearish Divergence | |

|---|---|---|

| Price | Makes a lower low | Makes a higher high |

| RSI | Makes a higher low | Makes a lower high |

| Meaning | Downtrend momentum weakening — potential reversal upward | Uptrend momentum weakening — potential reversal downward |

| Where found | Only at bottoms (in downtrends) | Only at tops (in uptrends) |

You can only look for bullish divergence in a downtrend (because you're looking for the bottom). You can only look for bearish divergence in an uptrend (because you're looking for the top). You can't find bearish divergence in a downtrend — it doesn't exist there.

Divergence Strength

There are three strengths of divergence — strong, medium, and weak. Strong divergences most often lead to major reversals. Weak divergences usually just produce a bounce.

Strong Divergence

- Bullish: Price makes a lower low, RSI makes a higher low

- Bearish: Price makes a higher high, RSI makes a lower high

- Most reliable — often leads to confirmed reversals

Medium Divergence

- Bullish: Price makes a double bottom (equal low), RSI makes a higher low

- Bearish: Price makes a double top (equal high), RSI makes a lower high

- Example: ASX Trader's Ethereum entry at ~$60 was based on medium bullish divergence (double bottom on price, higher low on RSI) + change of market structure through support

Weak Divergence

- Bullish: Price makes a lower low, RSI makes a double bottom (equal low)

- Bearish: Price makes a higher high, RSI makes a double top (equal high)

- Least reliable — more often leads to just a bounce followed by continuation, rather than a full reversal. Be careful if it rejects and keeps going

Steps to Find and Confirm Divergence

Step 1: Identify the Swing Points

Connect two low points on price (A and B). Then find the corresponding two swing lows on RSI. Are they going the same direction or opposite? If opposite = divergence.

Use the vertical line tool to match price pivots with RSI pivots — ensures you're looking at the right corresponding points.

Step 2: Assess Divergence Strength

Is it strong (lower low / higher low), medium (equal low / higher low), or weak (lower low / equal low)?

Step 3: Wait for Confirmation — DON'T Trade the Signal

Divergence alone is NOT an entry signal. It's an early warning. You need price action confirmation:

- A reversal pattern (failure swing, non-failure swing, double bottom)

- A change of market structure (HH/HL)

- A breakout through resistance or trend line break

- Even better: a combination of multiple confirmations

Step 4: Trade the TRIGGER, Not the Signal

The blinker analogy: Divergence is like a car's indicator/blinker. It signals the car is going to turn. But if you drove based on blinkers alone, you'd have an accident within a week — people put blinkers on wrong, too early, or not at all. Same with divergence. Sometimes the first divergence leads to a reversal. Sometimes it's the second, third, or fourth. You wait for the car to actually turn (change of market structure) before you act.

Signal = divergence. Trigger = change of market structure / reversal pattern / breakout. We trade triggers, not signals.

Do's and Don'ts for Drawing Divergence

Do's

- Draw divergence lines on extremes only (clear pivot points). The sharper the extreme, the better

- It's desirable for the first RSI extreme to be in the overbought or oversold zone (not in the middle of the range). Divergence from an extreme is more powerful

- The bigger the angle between the price line and the RSI line, the stronger the divergence

- Draw lines on candle bodies, not wicks — RSI follows bodies, not shadows

- Be consistent: if you connect two highs on price, connect the two corresponding highs on RSI. Use vertical lines to verify alignment

- Longer timeframes produce more reliable divergence. Monthly and weekly have fewer false signals than daily or hourly. Weekly divergence that builds over months signals something big (e.g. the S&P weekly bearish divergence before Trump tariffs and before COVID)

- Divergence isn't confirmed until a pivot is in. Until then, it's just potential divergence. You need the RSI to actually pivot for the divergence to be valid

- You can only count divergence after a "reset." RSI needs to have gone from one extreme to the other before you can start counting new divergence

Don'ts

- Don't trade divergence alone — wait for the trigger (price confirmation)

- Don't expect hourly divergence to produce a weekly-level reversal. Match your expectations to your timeframe

- Don't use multiple indicators that measure the same thing (e.g. RSI + MACD + Stochastic RSI = all price momentum). That gives you confirmation bias, not confirmation. They're all telling you the same thing in different ways

- Don't try to pick the exact top or bottom off divergence. "The glamour of wanting to pick the top or bottom is more about ego than profits"

Combining RSI with OBV

RSI measures price momentum. OBV measures volume momentum. These are different things, so using both is valid (unlike RSI + MACD which are both price momentum).

The ideal setup: RSI divergence confirmed by OBV divergence = two different signals both pointing the same direction. Enter on the change of market structure, hold until you get the opposite signal from either RSI or OBV.

This is what confluency means — multiple independent signals all telling you the same thing. The more confluency, the higher probability the trade works.

Craig's Key Insight: News Creates Catalysts for Moves That Were Already Due

The S&P 500 showed significant bearish divergence on the weekly timeframe before both the Trump tariff sell-off and COVID. The divergence was already signalling weakness — the news event just created the catalyst that expedited the pullback. "We were always going to pull back. The catalyst of the news made it happen much quicker."

This is why divergence is so powerful as a leading indicator — it shows you the setup before the trigger event occurs. By the time the news hits, the weakness was already there for weeks or months.

1.6 - Fibonacci & retracement zones

Understanding Fibonacci

The Fibonacci sequence — 0, 1, 1, 2, 3, 5, 8, 13, 21, 34, 55, 89… — is a series where each number is found by adding the two before it. Identified in the 13th century by Leonardo Fibonacci, though the sequence was known and used hundreds of years before (even in Egyptian architecture).

The Golden Ratio

The golden ratio 0.618 (or its inverse 1.618) is derived from the Fibonacci sequence and appears throughout nature — from atoms to galaxies, honeybee populations (female/male ratio = 1.618), sunflower spiral rotations, and even human body proportions (shoulder to fingertips ÷ elbow to fingertips ≈ 1.618). It's been used for centuries in art (Mona Lisa), architecture (pyramids), and design (Twitter logo).

The Fibonacci Levels

Dividing a number by the next in the sequence gives the key ratios:

- 21 ÷ 34 = 0.618 (61.8%)

- 21 ÷ 55 = 0.382 (38.2%)

The key retracement levels: 0%, 23.6%, 38.2%, 50%, 61.8%, 78.6%, 100%

Note: The 50% level is NOT actually a Fibonacci number. It's included because of Dow and Gann theory — and human psychology. If you see a "50% off" sale, you automatically gravitate towards it. Financial markets work the same — when something is half price, people perceive it as a bargain.

Fibonacci Retracement Strength — The "Discount" Framework

Each Fib level tells you something about the strength of the underlying trend. Think of it as a sale:

| Fib Level | Discount | Trend Strength | Meaning |

|---|---|---|---|

| 23.6% | ~24% off | Very strong | Buyers jumping in at a tiny discount — massive demand |

| 38.2% | ~38% off | Strong | Buyers stepping in at a modest discount — still strong demand |

| 50.0% | 50% off | Normal | Human psychology — half price attracts buyers naturally |

| 61.8% | ~62% off | Weak | Buyers waiting for a big discount before stepping in |

| 78.6% | ~79% off | Very weak | Needs to be nearly 80% off before anyone's interested |

| Below 100% | Full retrace | Reversal | No discount is enough — trend is over |

The key insight: If successive retracements go deeper and deeper (38.2 → 50 → 61.8 → break), the trend is weakening. Each time, buyers need a bigger discount before stepping in. When even an 80% sale won't attract buyers, the trend is done. This is how you can use Fibonacci to see a trend weakening before it fully reverses.

Example: Bitcoin showed successive retracements getting deeper — 382, then 500, then 618, then broke entirely. The trend was weakening with each leg, and Fibonacci showed it clearly.

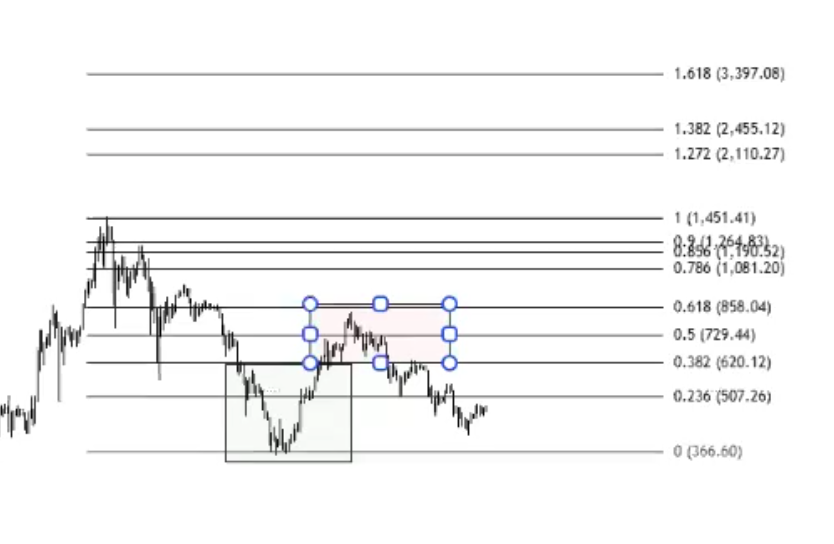

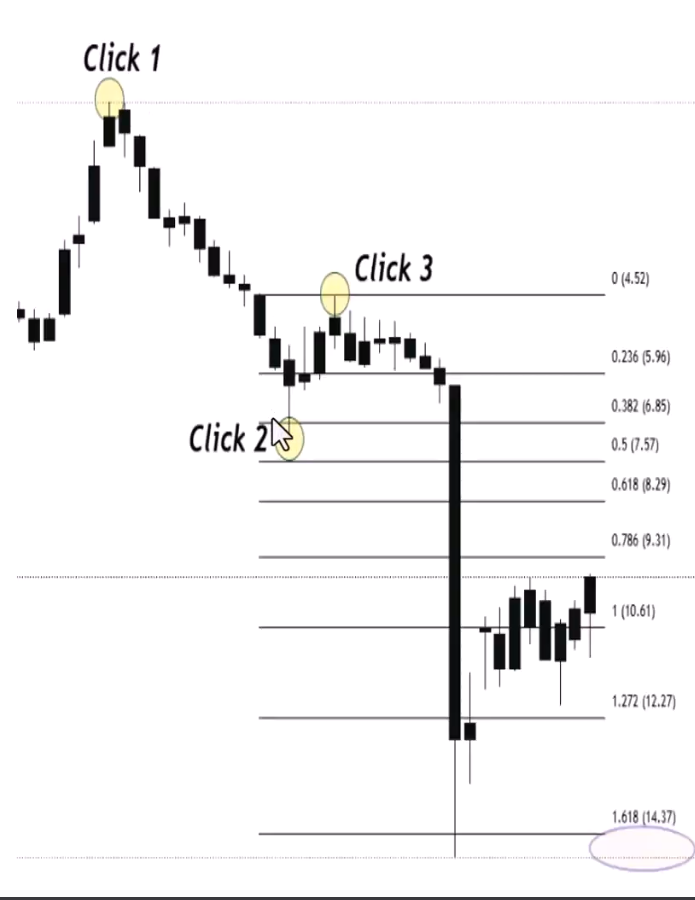

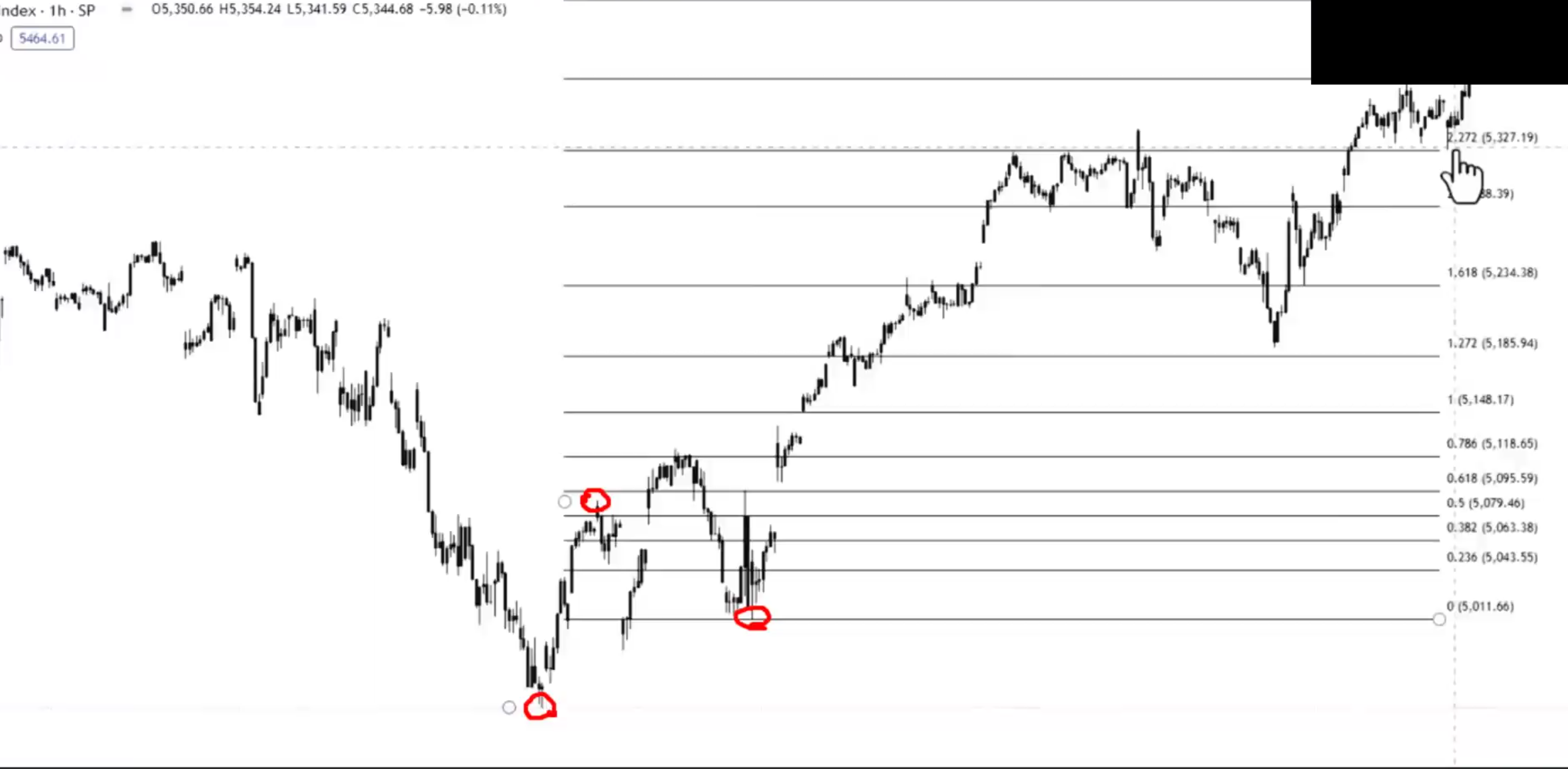

How to Draw Fibonacci Retracement

In TradingView: Left toolbar → 2nd group down → arrow → Fib Retracement (or Alt+F shortcut).

In an Uptrend (Looking for Support)

- Identify market structure is bullish (HH/HL)

- Find the major swing low and major swing high

- Click from the low (100%) to the high (0%) — wick to wick

- The levels show where you can expect support on the pullback (23.6, 38.2, 50, 61.8, 78.6)

In a Downtrend (Looking for Resistance / Profit Targets)

- Identify market structure is bearish (LL/LH)

- Find the major swing high and major swing low

- Click from the high to the low

- The levels show where you can expect resistance on the bounce (where to take profit)

Critical Rule: Draw Wick to Wick

Always draw from the wick of the low to the wick of the high (or vice versa). Not candle bodies.

The Golden Pocket — The Zag Zone

The 382-618 zone is called the "golden pocket" or the "zag zone." This ties directly back to Dow Theory: the secondary action is a 1/3 to 2/3 retracement of the primary move. The Fibonacci 382-618 range IS that 1/3-2/3 zone.

Nine times out of ten, the zag will come down to the golden pocket.

Every zag (correction) in a trend should retrace back to somewhere in the 382-618 zone. This is where you look for:

- Support in an uptrend (buying opportunity)

- Resistance in a downtrend (profit-taking / exit point)

Using the Zag Zone for Profit Taking

The zag zone isn't just for entries — it's essential for exits. In a downtrend, when price bounces, expect the bounce to reach the 382-618 zone of the prior down move. That's where you take profit or look for weakness, because the bounce may just be a zag before more downside.

Only two things can happen at the zag zone:

- It's just a zag (correction) and the prior trend resumes → price rejects at 382-618

- It's the beginning of a new trend → price pushes through the 618 on increasing volume

If price gets above the 618 on strong volume, it becomes more likely the bottom is in and a new bull market is starting. Until then, treat every move into the zag zone as potentially just a correction.

The Forecasting Process

- Identify your zone — draw Fib from the move, mark the 382-618 zag zone

- Watch for weakness when price reaches the zone — bearish divergence on RSI and OBV, declining volume, reversal candlestick patterns

- Wait for confirmation — change of market structure (reversal pattern) at the zone

- React — take profit, exit, or enter based on the confirmed setup

If price retests the zag zone, drops out, then retests the bottom of the zone again — that's usually a sign the price will continue to fall away.

The Bread and Butter Setup — Combining Everything

ASX Trader's process for entries:

- Price moves into a Fibonacci support level (382, 500, or 618)

- The move into the level happens on lowering volume

- Bullish divergence appears on OBV

- Bullish divergence appears on RSI

- A change of market structure confirms the reversal (double bottom, failure swing, or non-failure swing)

That's the complete setup — Fibonacci level + weakening volume + OBV divergence + RSI divergence + reversal confirmation. Don't just buy because it's on a Fib level. Combine everything from the prior five weeks.

How Markets Move: Zigs, Zags & Three Steps Forward

The Zig-Zag Pattern

Markets never move in straight lines. They zig (move in the trend direction) and zag (retrace). The zag comes back to the golden pocket (382-618) before the next zig.

Apple example: From the tech bubble bottom in 2003, every single correction came down to the golden pocket zone — 618, 500, 618, 618, 382, 618 — and bounced. Knowing the golden pocket for a strong fundamental company like Apple, Microsoft, Google means knowing where to look for buys.

Three Steps Forward, Two Steps Back (Simplified Elliott Wave)

The market moves in a rhythm: one, two, three forward — then one, two back.

Each forward move consists of:

- Zig 1 → Zag 1 (golden pocket) → Zig 2 → Zag 2 (golden pocket) → Zig 3

That gives you three zigs with two zags between them. After the third zig:

- The market doesn't just correct the last zig — it corrects the entire three-zig move

- The correction comes back to the golden pocket of the WHOLE move (typically to the bottom of the "wave 4" area — the bottom third of the final zig)

Connecting to Dow Theory Phases

The three zigs ARE the three phases:

- Zig 1 = Accumulation (breakout from the base)

- Zig 2 = Public Participation (the big trending move)

- Zig 3 = Excess (the blow-off top)

- Then the whole-move correction = Distribution/Bear market (corrects back 1/3-2/3 of the entire move from accumulation bottom to excess top)

This pattern repeats fractally: three small zigs make one medium zig, three medium zigs make one large zig, and so on. The major correction events (tech bubble, GFC, COVID) are the "two steps back" from the bigger three-step pattern.

Fibonacci Clusters (Advanced Confluency)

A Fibonacci cluster is when multiple Fibonacci levels from different timeframes or different moves overlap at the same price area. This creates a much stronger support/resistance zone than any single Fib level.

How to Find Clusters

- Draw Fib retracement on the recent move (e.g. daily timeframe, COVID bottom to top)

- Zoom out and draw another Fib retracement on the larger move (e.g. monthly timeframe, entire trend)

- Look for where levels from both overlap — e.g. the 618 from the recent move aligning with the 382 from the whole move

- Draw a rectangle box around the cluster zone — that's your high-probability support/resistance area

Microsoft Example

The 618 retracement from the COVID bottom overlapped with the 382 from the entire move. This created a cluster zone. Microsoft (a trillion-dollar company) bounced off this cluster zone — two independent Fib levels both pointing to the same area of support.

Cluster zones are stronger than single Fib levels because you have multiple independent mathematical reasons to expect support/resistance at that price.

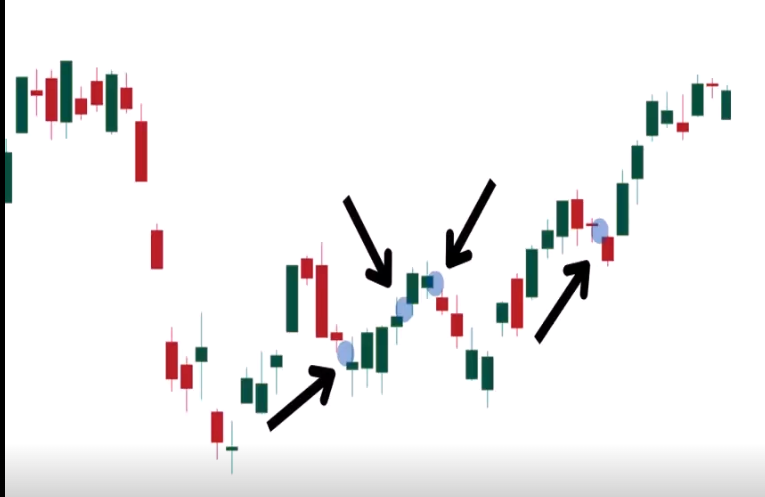

1.7 - Candlestick & Pattern Analysis

What Type of Trader Are You?

Before diving into candlesticks, you need to know which timeframe suits your personality. The candles you look at depend entirely on your trading style.

| Style | Timeframe | Hold Period | Risk | Reward | Stress | Best For |

|---|---|---|---|---|---|---|

| Position Trader | Weekly / Monthly | Months to years | Low | Low (slow) | Low | Long-term investors, relaxed personality |

| Swing Trader | Daily / Weekly | Days to weeks/months | Low-Med | Medium (takes time) | Low-Med | Patient traders, don't need daily results |

| Day Trader | 5min / 15min / 1hr | Within the day | Med-High | Higher (faster) | Higher | People who thrive on pressure |

| Scalper | 1min / 5min | Minutes to hours | High | High (immediate) | Very High | Adrenaline lovers, decisive under pressure |

Key insight: Your personality determines which style works. If you love roller coasters and spontaneity → scalping/day trading. If you prefer the beach and reading → swing/position trading. The educator started as a day trader (loved the rush, got fast feedback for learning), then transitioned to position trading as his life and priorities changed.

Match your chart timeframe to your style: Position trader = weekly/monthly. Swing trader = daily/weekly. Day trader = daily/hourly. Scalper = 1min/5min.

Anatomy of a Candlestick

Each candle gives four pieces of data: Open, Close, High, Low.

- Body = range between open and close

- Wicks/Shadows = the high and low extremes the price reached during the period

- Green/White = closing price was HIGHER than opening price (bullish)

- Red/Black = closing price was LOWER than opening price (bearish)

Multi-timeframe unpacking: A single daily candle can be unpacked by looking at the hourly/5min charts within that day. A bullish engulfing on the daily might show a clear downtrend reversal on the hourly. A bearish shooting star on the daily might show a strong downtrend on the 1-minute. This helps you understand what's actually happening inside each candle.

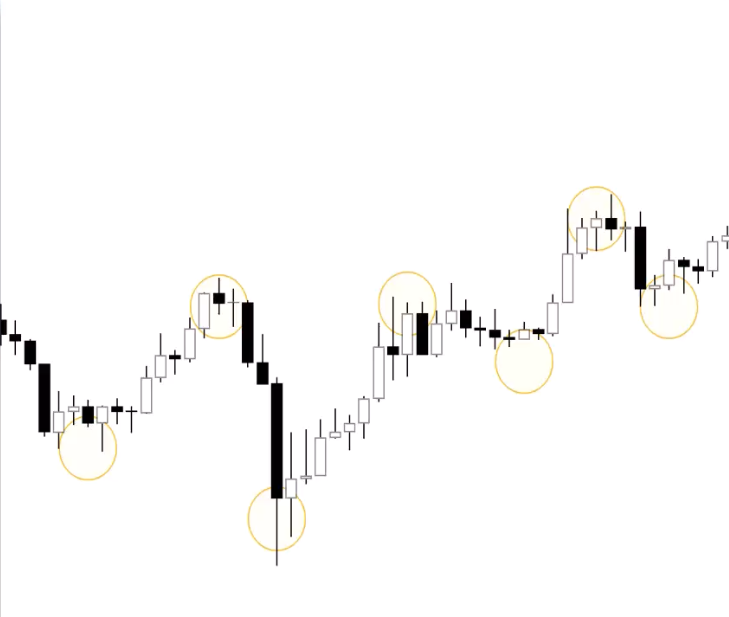

Candlestick Patterns

Reference Charts

| Bullish | Bearish |

|---|---|

|

|

|

|

|

|

No pattern works all the time — they represent tendencies, not guarantees. Always confirm with volume and other indicators.

Single Candle Patterns

Marubozu ("Bald Head"): No or minimal wicks — open/close IS the high/low. Bullish marubozu = intense buying pressure throughout the session. Bearish marubozu = intense selling pressure. These are powerful trend confirmation candles.

Hammer / Shooting Star: Long wick at one end, small body. Hammer (bullish) = long lower wick at bottom of downtrend, buyers stepped in hard. Shooting Star (bearish) = long upper wick at top of uptrend, sellers pushed price back down. Can be either colour.

Spinning Tops / Dojis: Short body centered between long upper and lower wicks. Neutral — represents indecision between bulls and bears. What matters is the candle that follows: big green after a doji = bulls won. Big red = bears won.

Multi-Candle Patterns

Bullish/Bearish Engulfing: Two candles where the second completely engulfs the first. Bullish engulfing at bottom of downtrend = reversal signal (buyers overwhelmed sellers). Bearish engulfing at top of uptrend = reversal signal. Look for high volume to confirm.

Inside Bar (Harami): Small candle completely inside the previous candle's range. Shows the trend is pausing — indecision. The next candle determines direction.

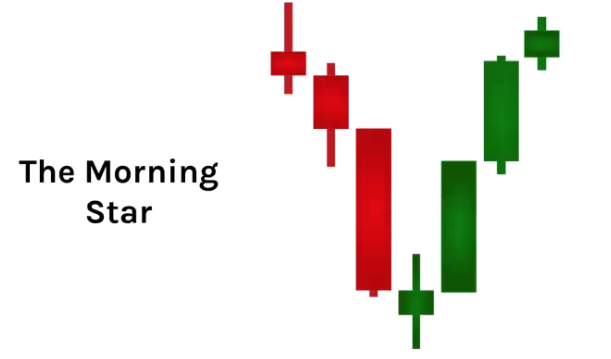

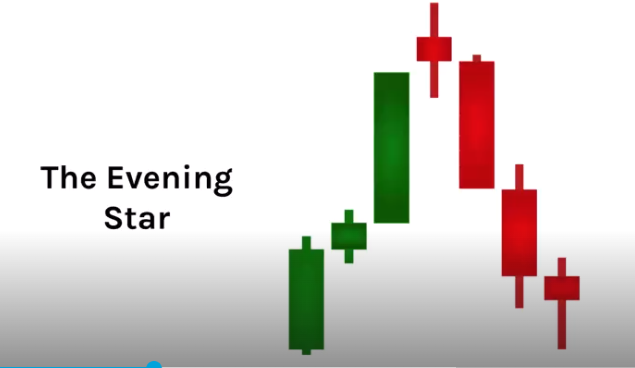

Morning Star / Evening Star: Three-candle reversal pattern. Morning star (bullish) = long red → doji/small body → long green. Evening star (bearish) = long green → doji/small body → long red. The doji shows the battle, the third candle shows who won.

Volume with Candlestick Patterns

- Reversal patterns (engulfing, hammers, stars) should have HIGH volume to confirm

- Climax/exhaustion candles at the end of trends often show extreme high volume

- Trend confirmation candles (marubozu) should be accompanied by strong volume in the trend direction

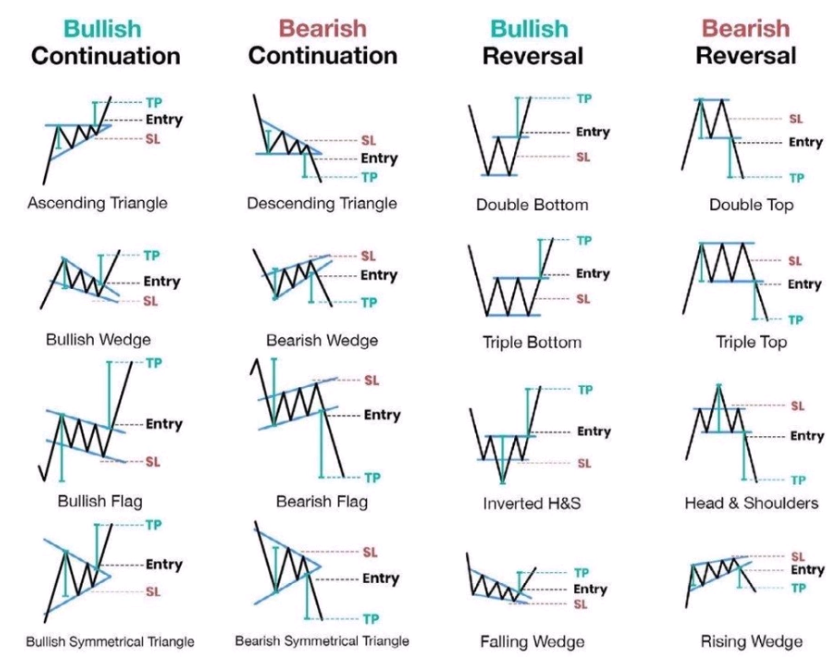

Chart Patterns

ASX Trader's honest take: "If I had to drop one lesson from the entire course, it would be this one." He's not a chart pattern trader — patterns can go either way and markets sometimes do the opposite because everyone is watching the same pattern. However, patterns complement other tools and provide useful common language.

The key principle: Don't just trade because you see a pattern. Unpack what's under the hood — it's all market structure. If you can identify pivot points and market structure, you don't technically need to know pattern names. But knowing the language helps communicate with other traders.

Continuation Patterns

Triangles

Converging price ranges showing a pause in the trend. Three types:

Symmetrical: Both lines converging at equal slopes. No directional bias — neutral consolidation. Direction depends on the breakout.

Ascending: Horizontal resistance + rising support (buyers stepping in higher each time). ~80% probability of upside breakout. Eventually sellers get exhausted.

Descending: Horizontal support + falling resistance (sellers stepping in lower each time). Eventually buyers get exhausted and it breaks down.

Elliott Wave connection: Triangles occur before the FINAL wave (wave 5 / excess phase). After a triangle breakout, expect one last push, then a correction. This is why triangle breakouts can trap retail traders — the move after the triangle might be short before rolling over.

Breakout vs fake-out: If a triangle breaks out and comes back within the pivot, it was likely a fake-out or a short excess phase. Check volume — breakout should be on high volume. Also check for divergence from the start to end of the triangle.

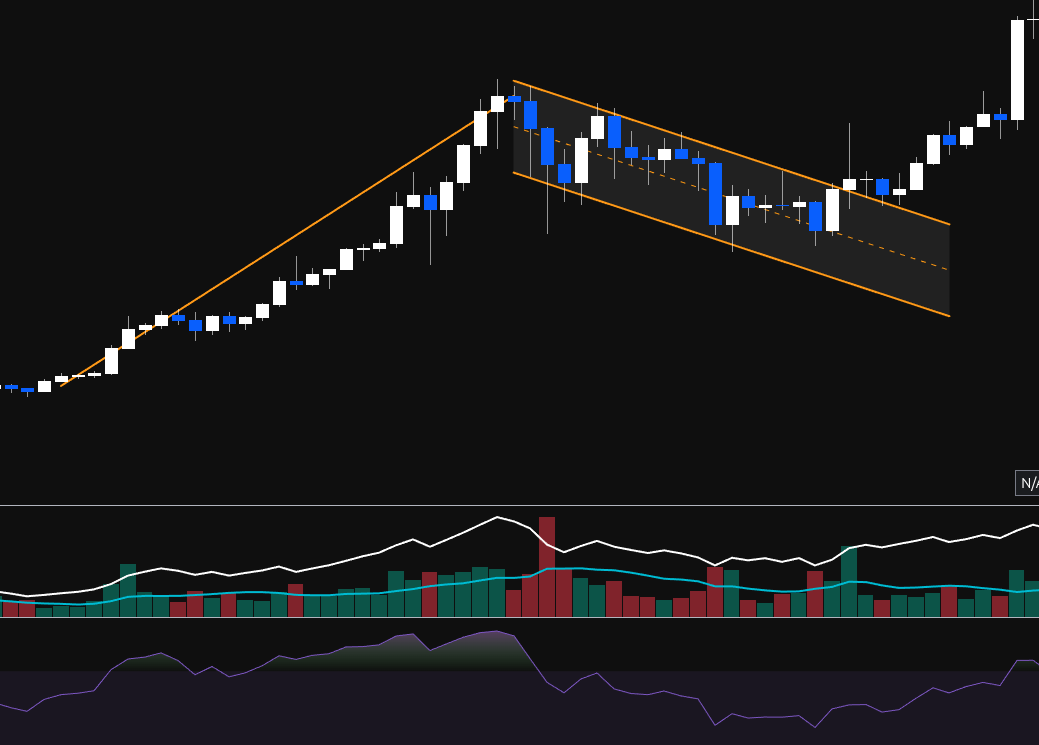

Flags & Pennants

Flags are short consolidation periods against the trend direction after a sharp impulse move (the "pole"). They're strong continuation patterns.

Bull Flag: Uptrend → sharp move up (pole, high volume) → consolidation down (flag, low volume) → breakout continuation (high volume). The flag should NOT retrace past the Fib 382 (maybe 500 max). If it goes to 618, it's too deep — it's not a flag, it's a weak trend.

Bear Flag: Downtrend → sharp move down → consolidation up to the zag zone (302-618) on low volume → breakdown on high volume.

Pennants: Same as flags but the consolidation forms a small symmetrical triangle instead of a channel. Also shouldn't retrace past 382.

Cup & Handle

Continuation pattern: prior uptrend → rounded bottom (the cup) → small pullback (the handle, which is basically a bull flag) → breakout. Handle should retrace to Fib 382, max 500. Handle must form on lowering volume. Breakout on increasing volume. Measured target = depth of the cup projected upward from the breakout.

Darvas Box (Rectangle)

Sideways consolidation with equal highs and equal lows. When it breaks out, check: is volume confirming? If breakout comes back within → liquidity grab (check OBV — was it going up on lowering volume?). If it breaks out and continues with strong volume → genuine breakout.

Reversal Patterns

Head & Shoulders / Inverse H&S

A head & shoulders is just a failure swing. Shoulder, head, shoulder = higher high, higher low, higher high, then lower high (the right shoulder fails to reach the head), then breaks the neckline.

Advanced H&S with volume and divergence:

- Left shoulder forms on increasing volume

- Head forms on LOWERING volume (weakness) + bearish divergence from left shoulder to head on RSI

- Right shoulder forms on LOWERING volume (dumb money buying the dip)

- Neckline break should come on increasing volume (sell pressure confirms)

- Measured target = distance from neckline to head

The neckline doesn't have to be horizontal — it can be diagonal.

Fractals: Each wave can have its own mini head & shoulders. Multiple small H&S patterns combine to form one large H&S (accumulation → public → excess → correction).

Wedges (ASX Trader's Favourite)

Converging trend lines both moving in the same direction (unlike triangles where they move in different directions).

Falling Wedge (Bullish): Both lines sloping down but converging. Tension builds as the trend tightens. Breakout to the upside on increasing volume. ASX Trader's favourite pattern — gives phenomenal risk:reward because you can enter on the breakout and place a tight stop loss. Target = back to the top of where the wedge started. Look for bullish divergence on both OBV and RSI as it comes down the wedge.

Rising Wedge (Bearish): Both lines sloping up but converging. Uptrend getting weaker. Should be going up on decreasing volume. Breakdown on strong volume.

Multi-Timeframe Candlestick Analysis

- Identify primary trend on higher timeframes (daily, weekly, monthly)

- Confirm on lower timeframes — look for consistent patterns aligning with the primary trend

- Spot entry/exit points on even lower timeframes (15min, 5min) for precise entries

- Detect confluences — a bullish reversal pattern on the daily, supported by a similar pattern on the 4-hour, with increased volume = strong setup

Example: A bullish engulfing on the daily = look inside and you might see a double bottom on the hourly. Two reversal signals confirming each other across timeframes.

Advanced Pattern Analysis — Combining Everything

The real power of patterns comes from combining them with volume and divergence:

For reversal patterns (H&S, wedges):

- Look for divergence on BOTH RSI and OBV as the pattern forms

- The reversal candles should have high volume

- The continuation into the pattern should show lowering volume (weakness)

- When you get divergence on price momentum AND volume momentum, plus a change of market structure = high probability setup

For continuation patterns (flags, triangles, boxes):

- The consolidation should happen on lowering volume

- The breakout should happen on increasing volume

- OBV should confirm the breakout (if OBV doesn't break out with price, it's likely a fake-out)

- Triangles = one more push before a correction (excess phase), so trade with awareness it might be short

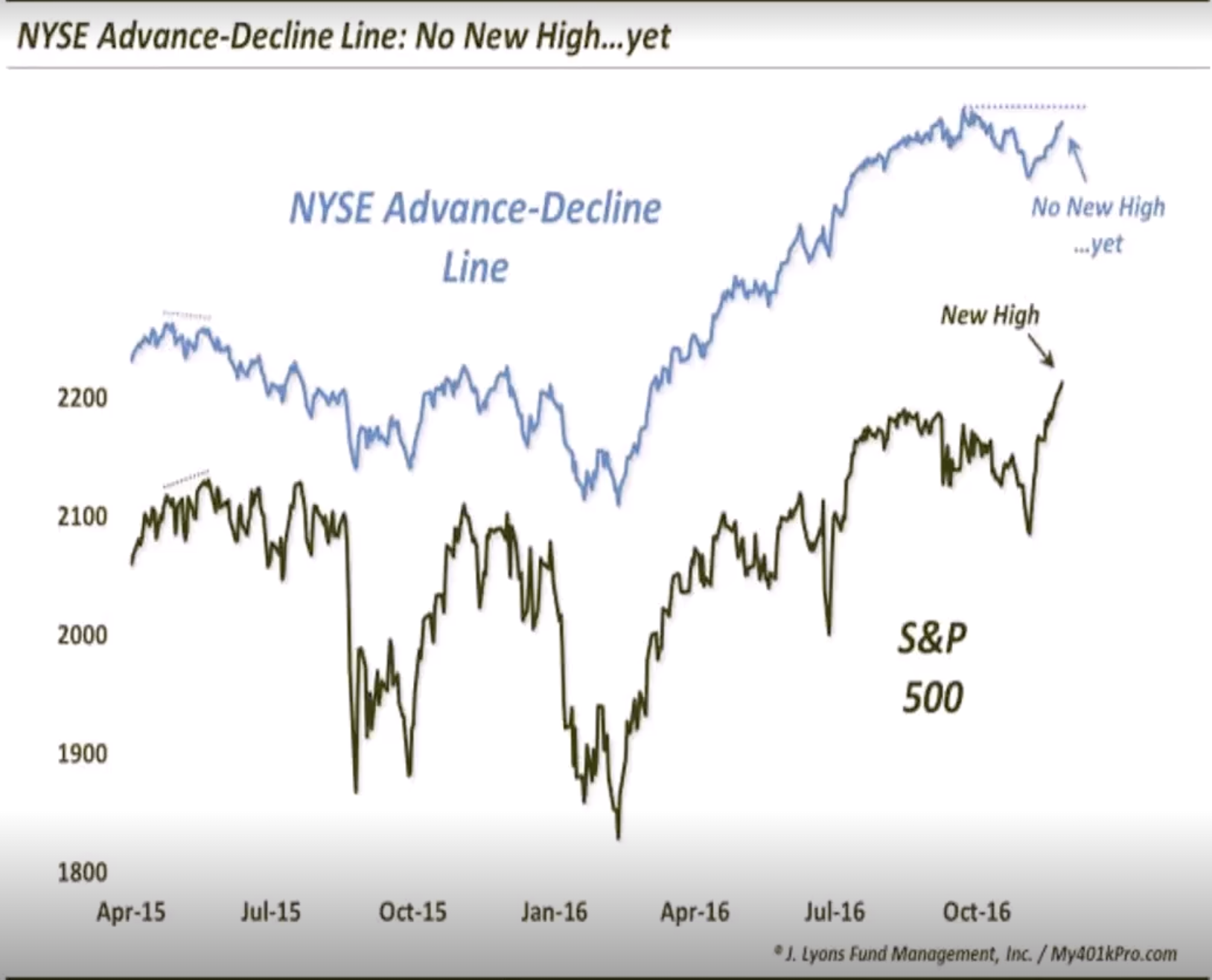

Index Confirmation

Dow Theory Tenet 5: The Averages Must Confirm One Another

For a market trend to be valid, both the Dow Jones Industrial Average (DJIA) and the Dow Jones Transportation Average (DJTA) must move in the same direction. If one average makes new highs while the other doesn't, it suggests weakness in the trend — divergence between indices is a signal (blinker) that a reversal may be coming.

Fun fact: Charles Dow invented both the DJIA and the DJTA. The DJIA is the longest-running American index (originally 12 stocks, now 30, over 100 years old). When someone questions TA, remind them the longest-standing American index is named after the guy who invented it.

Historical DJI vs DJT Divergence — 6 out of 6 Major Tops

The educator demonstrated that EVERY major market top showed DJT divergence before the crash:

- 1987 Crash (worst crash in history) — DJI making new highs, DJT making new lows. Change of market structure on both confirmed → could have avoided the biggest crash in history

- 1989-90 Crash — DJI new highs, DJT new lows before ~25% drop

- 2000 Tech Bubble — DJI new high in Jan 2000, DJT had already made a lower high from May 1999

- 2007 GFC — DJI new high, DJT made new low. Before the dramatic drop

- COVID 2020 — DJI making higher highs, DJT making lower lows before the crash

- 2022 Bear Market — DJI new highs, DJT making lower highs during the top

Six out of six times before a major crash, the transportation average was a leading indicator showing non-confirmation. This is a third type of divergence (alongside RSI price divergence and OBV volume divergence).

How to Compare in TradingView

- Click the layout selector (top right corner, small box icon)

- Select split screen (two charts side by side)

- Type the second ticker (e.g. DJT) in the right panel

- Match timeframes on both charts — make sure both are daily, or both weekly

- Use vertical lines to align pivots and dates across charts — this shows you whether the highs/lows match

Modern Multi-Chart Confirmation

Dow only had two indices to compare. Today there are many. The same principle applies: if you're in a raging bull market, ALL related indices should be raging and making new highs at the same time.

S&P 500 vs Russell 2000

The Russell 2000 (small caps, IWM) should confirm the S&P 500 in a healthy bull market. If the S&P keeps making new highs but the Russell goes sideways or makes lower highs, that part of the trend is weakening — money isn't flowing into risk-on small caps.

Bitcoin vs Ethereum

Ethereum is a more risk-on asset than Bitcoin. In a healthy crypto bull market, both should be making new highs. Examples of non-confirmation:

- BTC bottom at $15K: Bitcoin made a new low, but Ethereum made a higher low → indices not confirming → bullish divergence signal that the downtrend was weakening

- BTC top at $64K: Ethereum made a new high, Bitcoin made a lower high → not confirming → weakness before the rollover

Sector → Individual Stock Flow