Another simple way to check market breadth is checking sectors or large - mid - small caps (like btc against others)

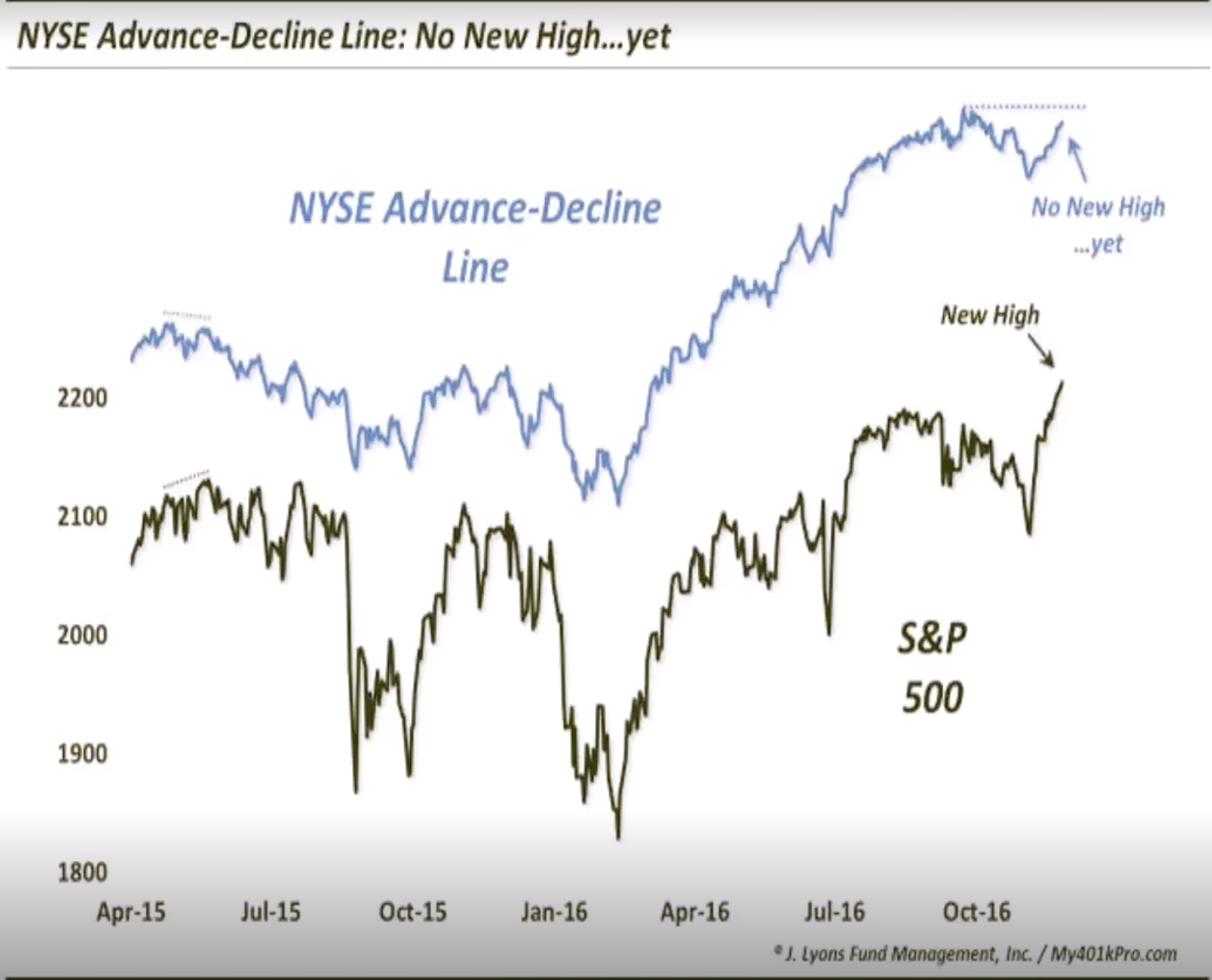

### AD line

- A line that is calculated by taking the difference between the number of advancing

- Can be used as a point of divergence, AD line may not have made a new high but price may have, signalling potential weakness

- Can be used like regular bearish / bullish divergence

[](https://pdb.conorbriggs.com.au/uploads/images/gallery/2026-02/lvg5miB3jY8dB6ao-image.png)

### Above / Below EMA Oscilator (ABO)

The ABO indicator is great to see if there is another point of divergence

[](https://pdb.conorbriggs.com.au/uploads/images/gallery/2026-02/wDeTYkBofHlGmb8x-image.png)

# Sentiment analysis

## Why Is Sentiment Important?

Sentiment reflects the collective emotions of market participants which can significantly influence market behaviour and price movements. Positive sentiment can drive buying pressure and negative sentiment can push price down. By analysing sentiment, traders and investors can predict potential market turning points, identify overbought and oversold conditions.

Understanding the behaviour of **RETAIL** investors and their tendency to crowd to one side of the market provides valuable insights. When retail sentiment reaches extremes and you anticipate potential market reversals, traders can PREPARE more effectively (tighten a stop loss, hedging).

Historical examples like the dot-com bubble, the 2008 financial crisis, and the cryptocurrency booms and busts highlight the impact of sentiment on market trends.

### Being on One Side of the Boat

When a majority of retail is bullish or bearish, the market often likes to move in the opposite direction. When everyone is bullish, most of the buying pressure has already been used up. When everyone is bearish, most people have already sold or are down so bad they are ready to capitulate.

Smart money use these extremes as signals to take the opposite position. With most investors already committed, there are fewer new entrants to continue driving the trend, leading to a reversal.

---

## Volatility Indexes (VIX)

The VIX (Volatility Index) reflects market sentiment. It is based on the S&P500 options market over the next 30 days. Expressed as an annualised percentage. Low VIX = low volatility expected (complacency). High VIX = high volatility expected (fear).

> **When the VIX peaks, this has often marked the bottom of the S&P500**

| Ticker | Measures Volatility Of |

|---|---|

| VIX | S&P500 30d options implied volatility |

| XVI | AU200 30d options implied volatility |

| BVIV | BTC 30d options implied volatility |

### VIX Key Levels & Historical Examples

- **Below ~18:** Bullish environment, everyone feeling comfortable

- **Above ~30:** Fear starting to come in

- **Above ~45-50:** Extreme fear / capitulation

**S&P 500 VIX extremes:**

- Oct 2008 (GFC bottom) — extreme VIX spike marked near the bottom (not exact, rolled slightly further before the actual bottom, but very close to capitulation)

- 23 March 2020 (COVID bottom) — VIX hit its high, marked the exact bottom

- Every other significant VIX spike (May 2010, Aug 2011, Aug 2015, late 2018, 2022) — each one marked at least a local bottom

**VIX breakout pattern:** Down, down, down, down → breakout above a declining trendline = volatility incoming. Look for breaks above declining resistance on the VIX as a warning of a correction ahead.

**Australian XVI:** Same concept. Single digits = very complacent (always ends in a spike). Above 20 = fear.

**BTC BVIV:** Above 75-100 = extreme greed (marked November 2021 top). Below 40-50 = fear (marked January 2023 bottom, August 2023 bottom).

---

## Sentiment Surveys

### AAII Sentiment Survey

Survey of individual investors measuring bullish/bearish/neutral expectations for the next **6 months** (not current sentiment — where they believe the market will be).

- **High 40s-50%+ bullish** = often marks a market peak. Time to be careful

- **High 40s-50%+ bearish** = often marks a market bottom. Potential buying opportunity

- Find it: Google "AAII sentiment" → first result

### NAAIM Exposure Index

Represents the **average exposure to US equities** reported by active investment managers (professional money managers, not retail).

- Shows how much institutional money is actually in the market

- **Look for convergence:** When NAAIM exposure matches price direction = healthy. When price goes up but NAAIM exposure drops = divergence (big money reducing exposure into the rally)

- Big money isn't always right, but it's worth knowing when they're reducing while retail is buying

- Find it: Google "NAAIM exposure index"

### Smart Money vs Dumb Money Confidence

Compares institutional investor behaviour ("smart money") with retail investor behaviour ("dumb money").

- When smart money is bullish and dumb money is bearish = potential buying opportunity

- When smart money is bearish and dumb money is bullish = potential selling signal

- **Look for divergence between the two lines** — when they diverge, something is about to change

- Retailers are emotionally driven, institutions are data driven

---

## Consumer Confidence Index (CCI)

The Consumer Confidence Index measures how optimistic or pessimistic consumers are regarding their expected financial situation and the overall economy. Based on surveys of a representative sample of consumers, used to predict consumer spending.

- **Above 100** = consumers confident, more inclined to spend

- **Below 100** = pessimistic, tendency to save more and consume less

- Extreme highs (tech bubble 2000, pre-GFC) often preceded recessions

- Extreme lows often aligned with market bottoms

- Find it: Google "consumer confidence index CCI"

---

## Fear & Greed Index

Two versions — CNN for stocks, Alternative.me for crypto.

- **Stock market:** Uses market momentum, stock price breadth, put-call options, market volatility, safe haven demand, junk bond demand

- **Crypto:** Uses volatility, market momentum, social media, surveys, dominance, trends

### Key Levels (Crypto)

- **Above 90:** Extreme greed / euphoria — often marks a local or major top

- **Below 10:** Extreme fear — often marks a local or major bottom

- Top 10% or bottom 10% = contrarian territory

Find it: Google "fear and greed index" — CNN (stocks) and Alternative.me (crypto) are the top two results.

---

## Put-Call Ratio & Options

### Put-Call Ratio

Compares the volume of put options (bearish bets) to call options (bullish bets).

- **Greater than 1** (more puts than calls) = bearish sentiment

- **Less than 1** (more calls than puts) = bullish sentiment

- **Around 1** = neutral/balanced

- **Contrarian indicator:** Extremely high ratio = market overly bearish, could rebound. Extremely low = overly bullish, could pull back

### Max Pain Theory

Max Pain is the price at which the largest number of option contracts expire worthless — causing maximum losses for option holders and minimum payouts for option sellers (Wall Street).

- The theory suggests price gravitates toward the Max Pain strike price at expiration

- Market makers may influence price toward Max Pain to maximise their profits (minimise payouts)

- It's always retailers vs Wall Street — Wall Street drives price to where they don't have to pay out billions

- Find it: Google "options max pain swaggy stocks"

### Triple Witching

Simultaneous expiration of stock options, stock index futures, and stock index options. Occurs **four times a year on the 3rd Friday of March, June, September, and December.**

- Leads to increased volatility and trading volume

- Index funds and institutional investors rebalance portfolios

- **Most major market tops and bottoms happen around these dates:**

- Tech bubble bottom: October (just after September witching)

- Tech bubble top: March

- GFC top: September/October

- GFC bottom: March 2009

- COVID bottom: March 2020

- 2022 bear market top: December/January period

**Always be careful for major turning points around end of March, June, September, December.** After expiration, people place new bets for the next quarter — these quarterlies are often inflection points.

---

## Advanced: Sentiment Divergence

Just like price vs RSI divergence, you can get divergence between **price and sentiment indicators.** When sentiment and price aren't matching, something is about to change.

### Bullish Sentiment Divergence

Price makes a **higher low** but sentiment makes a **new low** (more fearful than before). If prices are holding up but people are MORE scared than last time → the bearish sentiment is overextended → potential reversal upward.

**Bitcoin example:** June 2022 low had extreme fear (below 10 on Fear & Greed). When Bitcoin made a new low in November, Fear & Greed only dropped to ~20 — a higher low in sentiment. Why weren't we as fearful on a new price low? → Divergence → marked the actual bottom.

**S&P 500 example (March 2023 banking crisis):** Silicon Valley Bank collapse, extreme fear sentiment. But price printed a higher low compared to the October 2022 low. News was terrible (extreme fear), but the chart wasn't confirming it with new lows → divergence between FA/news and TA → continuation upward.

### Bearish Sentiment Divergence

Price makes a **new high** but sentiment makes a **lower high** (less greedy than before). Why isn't there euphoria if we're at new highs? → The bullish sentiment is fading → potential reversal downward.

### The Rule

If the news is really bad, the charts should be making new lows. If they're not → divergence. If the news is really good, the charts should be making new highs. If they're not → divergence. When FA/news says one thing but TA says another, trust the TA and look for the divergence to resolve.

This applies to individual stocks too — if terrible news comes out but the stock makes a higher low, that's bullish divergence between fundamentals and technicals.

# Fibonacci extensions

**Purpose:** To set price targets & support/resistance levels. While Fib retracements measure where price might **retrace** to, extensions project where price might **extend** to.

Fib extension levels expressed as ratios:

- **1.0 ← Important** (typical C wave extension)

- 1.272

- **1.618 ← Important (strongest magnet)**

- 2.0

- **2.618 ← Important**

- 3.618

- 4.236

- 4.618

Just because price hits an extension level doesn't mean you automatically sell, but it can be a stronger sell signal if you see weakness approaching or hitting the zone.

If it's a weak move (corrective wave), the C wave usually only hits 1.0 or 1.618. In a parabolic trend, switching to log scale is highly recommended.

---

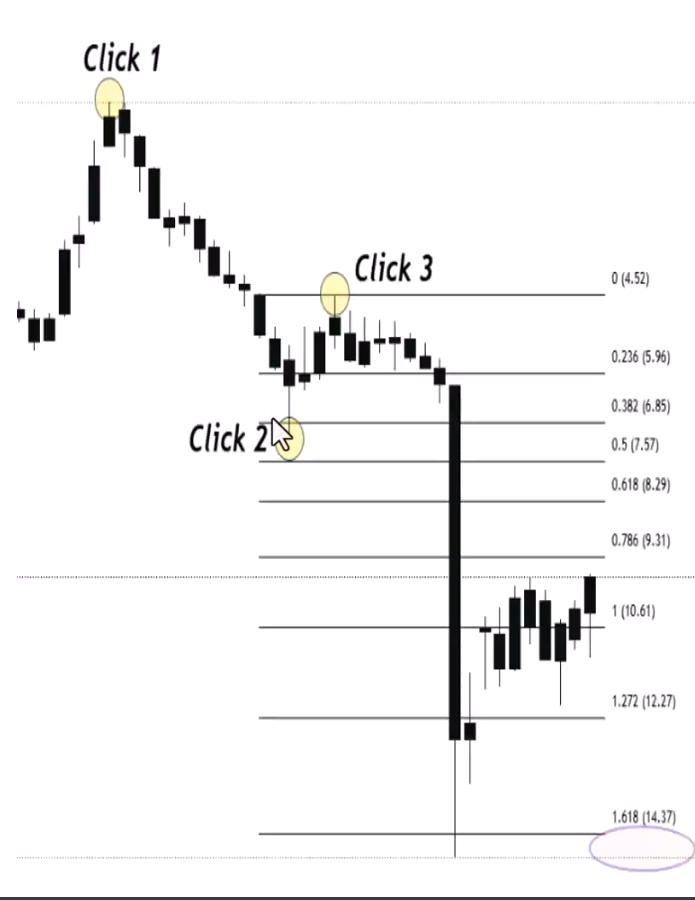

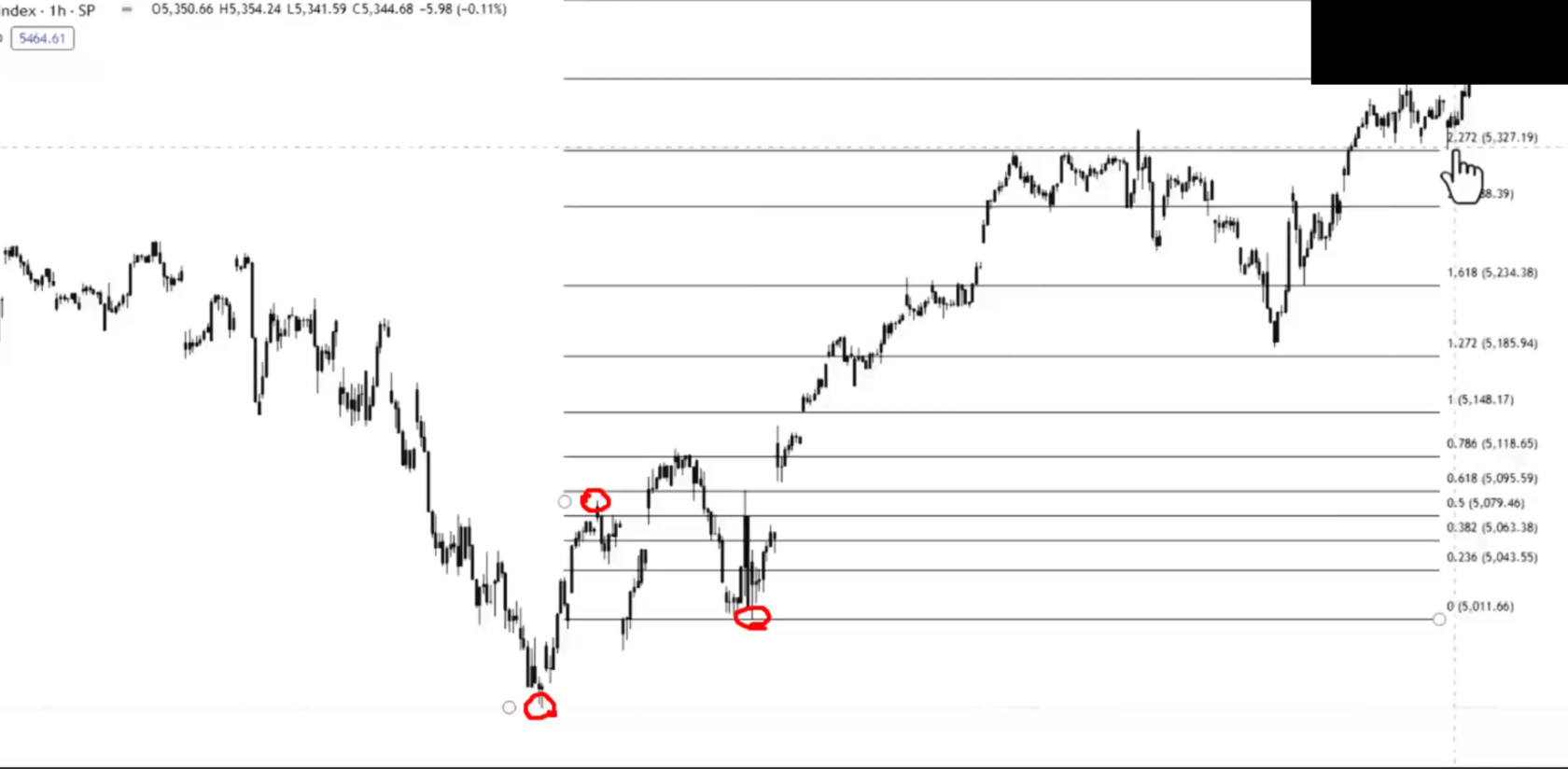

## How to Draw Extensions

**Three clicks:** Swing low → swing high → next swing low (for projecting upside). You're selecting from the start to the end of the correction — not just swing high to low to high.

[](https://pdb.conorbriggs.com.au/uploads/images/gallery/2026-04/qdy2dSazb2McHEyX-image.png)

[](https://pdb.conorbriggs.com.au/uploads/images/gallery/2026-04/DYURedQ8WrWtLatc-image.png)

[](https://pdb.conorbriggs.com.au/uploads/images/gallery/2026-05/yVcNHOpO3UZNjGHE-image.png)

---

## How Markets Move — Retracements + Extensions Together

The full cycle of using Fibonacci in a trending market:

**Wave 1 (Accumulation breakout):** First push up. Once it finalises, expect a deep retracement — typically down to the 618 or even 786 zone. Why deep? Nobody knows it's wave 1 yet — sentiment is still bearish, they think it's just a continuation of the downtrend.

**Wave 2 (Deep zag):** Comes down to the 618 zone. Once it bounces and takes out the wave 1 high, you can draw your **trend-based Fib extension** (bottom → top → pullback low) to project the next target. The **1.618 is the most common target** for the next leg.

**Wave 3 (Public participation):** Extends up to the 1.618 target zone. Then you get another retracement — but this time it's typically shallower (382 or Fib 500) because the trend is now established and stronger. If wave 2 was deep, wave 4 is usually shallow (and vice versa).

**Wave 4 (Shallow zag):** Comes down to the 382 zone. Once it bounces and takes out the wave 3 high, draw another extension to project wave 5's target.

**Wave 5 (Excess):** Extends to the target, then you get the big correction of the whole move.

### The Critical "Past the Zag Zone" Signal

If price comes down to the zag zone (382-618) and bounces = healthy, all good. But if it then rolls over, changes market structure, and breaks through the resistance-turned-support:

1. You're NOT just retracing the last move — you're retracing ALL of it

2. Get out the Fib retracement from the ENTIRE move (bottom of wave 1 to top of wave 5)

3. Look for support in the 382-618 of the whole move

4. Once buyers step in there + change of market structure + break back above the decline = re-entry

**"The minute we go past the zag zone and resistance didn't become support, I know I'm not just retracing from here — I'm retracing all of it."**

---

## The Repeating Process

1. **Retracement** to find buy zones (where will the zag end?)

2. **Extension** to find targets (where will the next zig reach?)

3. Check Fib strength (236 = very strong, 382 = strong, 500 = normal, 618 = weak)

4. Repeat at each new zig-zag

5. When the zag goes too deep (past the zag zone) → switch to retracing the whole move instead of just the last leg

**70-80% of the time, buyers step in at the zag zone.** The probabilities are in your favour. When they don't, the probabilities shift — and that's when you don't want to be trading it. Always trade probabilities — stack the chips, become the casino.

# 2.10 - Fibonacci clusters & extension channels

## Advanced Fibonacci Clusters

In Term 1, you learned clusters from multiple retracements on different timeframes overlapping. Now you're combining **retracements AND extensions** at the same zone — the ultimate cluster.

### What Are Advanced Clusters?

When a Fib retracement level (e.g. 382 from the whole move) aligns with a Fib extension level (e.g. 1.618 from the last ABC correction) at the same price area = extremely high-probability support or resistance zone.

You're getting two completely independent Fibonacci calculations pointing to the same price. That's not coincidence — that's the market telling you something.

### Steps to Identify

1. **Identify the trend** — determine the significant high and low points

2. **Draw Fib retracement** from the start of the whole move to the end — mark the 382, 500, 618 zones

3. **Draw Fib extension** from the last ABC correction (top → bottom → retracement high) — mark the 1.0, 1.618, 2.618 levels

4. **Find the clusters** — look for where retracement and extension levels converge at the same price area

### Ethereum Example — Calling the Bear Market Bottom

The educator demonstrated this on Ethereum's bear market:

1. Price changed market structure bearish. Drew Fib retracement from the whole uptrend → identified the 382, 500, 618 as the zag zone for the entire move

2. Price bounced off the zag zone of the last leg but then broke through → not just retracing the last move, retracing ALL of it. Switched to the full-move retracement

3. Drew Fib extension from the ABC pattern (top → bottom → B wave retracement) → the **1.618 extension landed at the exact same price as the 382 retracement**

4. That became the high-conviction zone — the Fib cluster of 1.618 extension + 382 retracement

**The bottom of Ethereum's bear market landed exactly on that cluster zone.** Two independent Fibonacci calculations both pointing to the same price = the ultimate confluency.

### Don't Just Put a Buy Order There

Even with a perfect cluster zone, you still need:

- **Weakness signals** coming into the zone (lowering volume, RSI divergence)

- **Change of market structure** off the zone (the car actually turning the corner)

- **Blinkers on + trigger confirmed** at the projected target

The cluster tells you WHERE it should turn. The indicators tell you it's WEAKENING into that zone. The market structure tells you it HAS turned. All three together = "you should be shocked when the trade doesn't go your way."

---

## Fibonacci Extensions with Channels

Combining Fib extension targets with trend channel boundaries gives you precision take-profit zones.

### How It Works

**Channels** = trendline + parallel line creating a range where prices oscillate. **Fib extensions** = projected price targets beyond a retracement. When the top (or bottom) of a channel aligns with a Fib extension level = high-probability rejection/take-profit zone.

### Steps

1. **Identify the trend** and draw your channel (connect higher lows for uptrend, draw parallel to form the channel)

2. **Draw Fib extension** from the same trend (bottom → top → pullback)

3. **Look for convergence** — where does a Fib extension level intersect with the upper or lower channel boundary?

4. That intersection = your take-profit target

### Uptrend Example

Channel drawn from higher lows with parallel at the highs. Fib extension from bottom → top → pullback showed the **1.0 level aligned with the top of the channel**. That's where you'd look for rejection and take profit. Two independent methods (geometric channel + Fibonacci mathematics) both pointing to the same price.

### Another Uptrend Example

Channel + Fib extension showed the **1.618 aligned with the top of the channel**. Price hit the 1.618, rejected at the channel resistance, then fell out of the channel + changed market structure. Three confirmations to exit:

1. Hit the Fib 1.618 target ✓

2. Rejected at channel resistance ✓

3. Changed market structure + fell out of channel ✓

**"Nail in the coffin — hit all our zones, channel resistance, Fib 1.618, change of market structure. See you later."**

### Downtrend Example

Works identically in reverse. Channel drawn from lower highs, Fib extension projected downward. The **1.618 aligned with channel support** = zone where you'd look to exit shorts or look for a reversal. When price hit the 1.618, bounced off channel support, and then changed market structure back out of the channel = trend over, look for a new direction.

### Key Points

- Extension + channel targets are **zones, not exact prices** — sometimes a little short, sometimes a little long

- The actual confirmation/trigger is when price **falls out of (or breaks above) the channel** after hitting the Fib target

- These tools give you the WHERE (target zone). Market structure gives you the WHEN (trigger)

- Can be combined with clusters for triple confluency: Fib retracement + Fib extension + channel boundary all at the same price

# Term 2 master class

## The Course Architecture — What's Non-Negotiable vs Complementary

### Term 1 Weeks 1-6: THE NON-NEGOTIABLES

Everything in the first six weeks is the foundation. If you're not doing ALL of these on every trade, you're missing a beat:

1. **Pivot points** → market structure identification (Week 1)

2. **Support & resistance zones** (Week 2)

3. **Failure swings & non-failure swings** → confirmed reversals and entries (Week 3)

4. **Volume & OBV** → supporting the move, effort vs result (Week 4)

5. **RSI divergence** → early warning signals (blinkers) before triggers (Week 5)

6. **Fibonacci retracements** → zag zones, trend strength, targets (Week 6)

### Term 1 Weeks 7-9: COMPLEMENTARY TOOLS

These add confluency but aren't essential for a trade to exist:

- Candlestick patterns, chart patterns (Week 7)

- Index confirmation, multi-chart confluency (Week 8)

- Market psychology, sentiment, contrarian investing (Week 9)

### Term 1 Week 10: RISK MANAGEMENT

Not about your entry — it's about how small your stop loss is. A later entry with a better R:R can be more profitable than an earlier entry with a wider stop.

### Term 2: ADVANCED REFINEMENT

All of Term 2 builds on the non-negotiables:

- **Three types of divergence** — regular (reversal signal), hidden (continuation signal), directionally aligned (same direction, different rates = early warning). Complex divergence is where regular and hidden battle each other

- **Multi-timeframe divergence** — hidden bullish on the higher timeframe (continuation) + regular bullish on the lower timeframe (reversal entry) = precise entry for a big move

- **Pattern recognition + divergence fusion** — hidden divergence for continuation patterns, regular divergence for reversal patterns. Volume rules are OPPOSITE for each

- **Moving averages** — SMA for long-term, EMA for short-term. Used as confluency, not standalone

- **Gaps** — common (always fill), breakaway (new trend), runaway (continuation), exhaustion (reversal), professional (institutional), fair value (crypto imbalances)

- **Market breadth** — looking under the hood to see if stocks are actually participating in the index move

- **Sentiment analysis** — VIX, AAII, Fear & Greed, put-call ratio. Contrarian at extremes

- **Fibonacci extensions & clusters** — projecting targets, combining retracements + extensions for ultimate cluster zones

- **Fibonacci extension channels** — combining Fib targets with channel boundaries for precision take-profit

---

## Log vs Linear — When to Use Each

**Linear (default, first port of call):**

- $10 move here = same size as $10 move there (dollar-based)

- Better for identifying accumulation/public/excess phases visually (accumulation looks flatter and longer, which is what you expect)

- Use for most standard analysis

**Logarithmic (for long timeframes and large price ranges):**

- 10% move here = same size as 10% move there (percentage-based)

- Much easier to see waves and chart detail when prices range from $3 to $50+

- Essential for crypto, uranium, lithium — anything with hundreds or thousands of percent moves

- Makes the detail of smaller early moves visible instead of being squashed at the bottom

### Fibonacci in Log vs Linear — BOTH Are Valid

This was a key insight from the masterclass. When applying Fib retracements:

- **Linear Fib 618** creates a resistance zone in dollar terms

- **Log Fib 618** creates a resistance zone in percentage terms

- **Both work as resistance** — and they're at DIFFERENT price levels

**Silver example:** In linear, the 618 retracement created a major resistance cluster at one level. In log, the 618 created resistance at a different level (the percentage-based retracement). Both levels acted as genuine resistance on the chart. So drawing Fibs in both modes gives you TWO valid zones to watch.

**Pro tip:** To apply Fib in log scale in TradingView, open the Fib tool settings and check "log scale."

### When to Switch

- Start in linear to identify phases and get the big picture

- Switch to log when dealing with very long timeframes, very large price ranges, or parabolic moves

- In log, a retracement that looks like 78.6% in linear might only be 50% in percentage terms — this changes your analysis of trend strength

---

## Phase Analysis — Equities vs Commodities

**In equities (tech, financials):** The public participation phase is typically the largest. Excess phase is usually smaller.

**In commodities (silver, gold, uranium):** The excess phase is often the biggest — bigger than public participation. Commodities tend to have blow-off tops.

**The alternation rule:** If public participation is very extended (long duration), don't expect excess to also be very extended. One will be extended, the other normal. You rarely get both dramatically extended.

---

## Wave 2 Deep / Wave 4 Shallow

- **Wave 2 retracements** are notoriously deep — 618, sometimes 786. Why? Nobody knows it's wave 1 yet. Sentiment is still bearish from the prior downtrend. Everyone thinks it's just a continuation of the bear market

- **Wave 4 retracements** tend to be shallower — 382 or Fib 500. The trend is now established and people are bullish, so they buy the dip earlier

This alternation is important for setting expectations and targets. If wave 2 was deep (618+), expect wave 4 to be shallow (382). If wave 2 was shallow (unusual), expect wave 4 to be deeper.

---

## Channels as Confluency

Channels (trend lines + parallel lines) provide confluence with other tools:

- **Maximise touches** when drawing channels — the more times price respects the channel boundary, the more valid it is

- **Channels don't beat S/R zones** — a horizontal support/resistance zone with many touches is still the strongest level. Channels complement S/R, they don't replace it

- When a channel boundary aligns with a Fib level AND a horizontal S/R zone = triple confluency

- **Break of channel + change of market structure + hit Fib target** = the trend is over. The "nail in the coffin"

### Three Channel Types (Preview for Elliott Wave)

1. **Base channel** — drawn from the start

2. **Trend channel** — drawn during the trend

3. **Final channel** — drawn at the end

These will be covered in depth during Term 3.

---

## The 50% Profit-Taking Strategy

When your trade hits the target zone:

1. **Take 50% off the table** — lock in profit, remove risk

2. **Let the other 50% run** — trail your stop loss and see where it goes

3. If it continues beyond the target = bonus gains with zero risk (you've already banked profit)

4. If it reverses = you've already taken half your profit and the trailing stop catches the rest

This removes the psychological battle of "should I sell all or hold all" — the answer is "both."

---

## Preparing for Term 3: Elliott Wave

Everything from Term 1 and Term 2 translates directly:

| What You Know | What It Becomes in Elliott Wave |

|---|---|

| Accumulation | Wave 1 |

| First zag (deep) | Wave 2 |

| Public participation | Wave 3 |

| Second zag (shallow) | Wave 4 |

| Excess phase | Wave 5 |

| Correction (2 steps back) | ABC correction |

The internal counts work the same way — within wave 3, there's its own 1-2-3-4-5. Within that sub-wave 3, there's another 1-2-3-4-5. Fractals all the way down.

**Corrections are where Elliott Wave gets really challenging** — there are many different types. The course spends 4-5 weeks just on corrections because that's the hardest part.

**The key thing you must feel comfortable with before starting Term 3:** Accumulation → public participation → excess. If you can confidently identify the three phases, the numbering is just labelling what you already know.

# Elliott Wave - General

### General

When an initial pump then dump happens, how do you know if its a 1-2 or A-B?

- You must prepare by thinking the first impluse could be a 1 OR A, 2 OR B, and 3 OR C.

- A C has a much lower target then a 3 (use fib extensions)

- You either get a motive or corrective wave.

- Motive takes you in the primary wave of the overall movement

- Corrective takes you away from the primary trend.

### Wave 1

---

### Wave 2

- On the wave 2 retracement, you usually target the 0.5 to 0.786 due to it being a deeper pullback and people are still in denial / fear that the pull back is a fake out

---

### Wave 3

- Minimum target using fib extensions is hitting or passing 1.618

- A wave 3 should breakout cleanly from a channel while a wave C usually stays within or may jump out and back in

---

### Wave 4

---

### Wave 5

---

### Wave A

---

### Wave B

---

### Wave C

- Minimum target for a C wave is 0.618 with an ideal target between 1 and 1.236. If it extends past the 1.236, then it's most likely a wave 3

- Usual extension of a C wave is 0.618 and 1.236

# EW notes

if the wave 1 is very powerful, it's likely the next waves won't be as big

\- wave 3 cant be the smallest, therefore wave 5 would have to be very small

EG SOL

[](https://pdb.conorbriggs.com.au/uploads/images/gallery/2026-05/malNXE4iEa6T6tgX-image.png)

wave 2 is usually very deep because the bag holders who bought at the top of wave 5 are looking for any opportunity to get out so they sell thinking the wave 2 is about to make a new lower low

# Elliott Wave — Impulse Waves

## Predictive vs Reactive TA

Everything learned previously (market structure, S/R, divergence, volume, Fibonacci) is **reactive** TA — adapting to real-time market conditions. Elliott Wave is **predictive** — identifying recurring patterns and forecasting future price movements based on crowd psychology.

Think of it like a military general: reactive TA is adapting to real-time changes in battle. Elliott Wave is studying the enemy's past behaviour to predict their next moves BEFORE the battle. The best Elliotticians combine both — they use Elliott Wave for the prediction and reactive TA (divergence, volume, S/R, market structure) for the confirmation.

**Critics mock Elliotticians for adjusting wave counts.** That's actually the point — you have a predicted roadmap, and when the market deviates, you adjust. The wave count tells you when you're wrong and how wrong. Having rules means you know exactly when your analysis is invalidated.

---

## History — Ralph Nelson Elliott

Developed in the 1930s by Ralph Nelson Elliott, an accountant who observed that markets trade in repetitive cycles driven by crowd psychology. He proposed that prices unfold in specific patterns: a **five-wave motive phase** in the trend direction, followed by a **three-wave corrective phase** against it. This eight-wave cycle repeats at every scale — fractals.

Being a Certified Elliott Wave Analyst (CEWA) or Master Certified (CEWA-M) is one of the most respected credentials in technical analysis.

---

## The Complete Cycle

One complete cycle = **8 waves:**

- **Motive phase (5 waves):** Labelled with NUMBERS (1, 2, 3, 4, 5) — moves in the direction of the trend

- **Corrective phase (3 waves):** Labelled with LETTERS (A, B, C) — moves against the trend

**Quick identifier:** Numbers = motive (with the trend). Letters = corrective (against the trend).

The motive phase contains three types: **impulse waves** (most common, covered here), **extended waves** (covered next), and **diagonal waves** (covered after that).

---

## The Five Impulse Waves

### Wave 1 — The Initial Move (Accumulation)

- Marks the beginning of a new trend, often after the previous trend has exhausted

- Rarely obvious at inception — sentiment is still bearish from the prior downtrend

- Lower investor confidence, market hasn't fully shifted yet

- Volume may be relatively low (sometimes high if institutional money enters)

- Often targets the zag zone of the previous correction (382, 500, or 618), or a 1:1 of the previous corrective wave, or 61.8% of the previous correction

- This is where you get your failure swings, non-failure swings, and inverse head & shoulders — the reversal patterns from the foundational course

### Wave 2 — Deep Correction

- Corrects wave 1 but **CANNOT retrace beyond the starting point of wave 1** (Rule #1 — not even by one cent, not even a wick)

- Typically a **deep** retracement: 50-61.8%, sometimes 78.6%

- Sentiment is still bearish — everyone thinks the bear market is still intact ("just another lower high")

- Volume tends to decrease (corrective move, lower participation)

- Often looks sharp and steep

- If wave 2 goes below the start of wave 1 → the count is INVALIDATED. Start over

### Wave 3 — The Strongest Wave (Public Participation)

- Typically the **most powerful and extended** wave (in equities — in commodities, wave 5 can be larger)

- Strong market sentiment and widespread participation

- Sharp and rapid price increase with high volume

- Corrections within wave 3 are short-lived and shallow — anyone waiting for a pullback misses the boat

- The centre of wave 3 often looks nearly vertical

- **Cannot be the shortest** of waves 1, 3, and 5 (Rule #2 — doesn't have to be the longest, just can't be the shortest)

- Common Fibonacci extension targets from wave 1: **1.618** (most common, ~60-70% of the time), **2.0**, **2.618**, or even higher in strong trends. Can also be 1.0 (equal to wave 1) in weaker trends

### Wave 4 — Shallow Correction

- Corrects wave 3 — usually **less severe** than wave 2

- Often takes the form of sideways consolidation (triangles, flats, choppy action)

- **Cannot overlap with the price territory of wave 1** (Rule #3 — exception: diagonal patterns)

- Typically a shallow retracement: **23.6-38.2%**, sometimes 50%. Rarely 61.8% (would risk overlapping wave 1)

- Volume well below wave 3

- Often frustrating — takes a long time, goes nowhere. "If you're feeling lost, you're probably in wave 4"

- Good place to buy a pullback if you understand wave 5 is coming

### Wave 5 — The Final Push (Excess)

- Last wave in the impulse sequence — driven by the final burst of enthusiasm

- News is universally positive, everyone is bullish

- Often shows **divergence** on RSI (weakening momentum from wave 3 to wave 5)

- Volume may **decline** compared to wave 3 — suggests trend exhaustion

- Average investors finally buy in right before the top

- Can sometimes **truncate** — fail to move beyond the end of wave 3 (double top, then reversal)

---

## The Three Cardinal Rules (CANNOT Be Broken)

| Rule | Description | If Violated |

|---|---|---|

| **1. Wave 2 cannot retrace more than 100% of wave 1** | Wave 2 cannot go below the starting point of wave 1 — not even by one cent | Wave count is invalidated — re-evaluate |

| **2. Wave 3 cannot be the shortest** | Wave 3 doesn't have to be the longest, but it cannot be shorter than BOTH wave 1 and wave 5 | Wave count is invalidated — re-evaluate |

| **3. Wave 4 cannot overlap wave 1** | Wave 4 cannot enter the price territory of wave 1 (exception: diagonal patterns) | If not a diagonal, wave count is invalidated |

### Additional Guidelines (Common But Not Mandatory)

**Wave Extension:** Usually one impulse wave (typically wave 3) will be significantly longer than the others. ~80-90% of impulse waves have at least one extended wave.

**Truncation:** Wave 5 sometimes fails to surpass wave 3 — creates a double top before reversing. Still a valid 5-wave count, just with a truncated wave 5.

**Channels:** Impulse waves often fit within parallel trend channels. Drawing a channel from wave 1 to wave 2, parallel to wave 3, can help identify wave 4 targets and wave 5 projections.

**Alternation Rule:** If wave 2 is simple/sharp (deep zigzag), expect wave 4 to be complex/sideways (flat, triangle). If wave 2 is complex, expect wave 4 to be simple. They should NOT look the same. This helps you anticipate what type of correction wave 4 will be based on what wave 2 looked like.

---

## Fibonacci Targets for Each Wave

### Wave 1 Targets

- 100% of the previous corrective wave (1:1)

- 61.8% of the previous corrective wave

- 38.2-61.8% retracement of the previous impulse (the zag zone)

### Wave 2 Retracement Levels

- **38.2%** — shallow, indicates very strong trend (less common for wave 2)

- **50%** — moderate correction

- **61.8%** — most common for wave 2 (deep correction, sentiment still bearish)

- **78.6%** — deep but still valid (cannot reach 100%)

### Wave 3 Extension Targets (from wave 1)

- **1.618** — the golden ratio, most common (~60-70% of the time)

- **2.0** — strong trends

- **2.618** — very strong trends

- **1.0** — equal to wave 1 (weaker trends — implies wave 5 must be small since wave 3 can't be shortest)

### Wave 4 Retracement Levels (of wave 3)

- **23.6%** — very shallow, strong trend

- **38.2%** — typical for wave 4

- **50%** — deeper but still common

- **61.8%** — rare, risks overlapping wave 1 depending on the wave structure

### Wave 5 Targets

- **Equal to wave 1** — the most common target (especially when wave 3 was extended)

- **61.8% of waves 1+3 combined** — very common. Measure wave 1 + wave 3 combined length, pull back to wave 4, project 61.8% = wave 5 target

- **1.618 of waves 1+3 combined** — for extended wave 5s (common in commodities)

- **100% of wave 3** — less common, occurs in strong trends

- **Real examples:** The educator called the exact top on Lake Resources using the 1.618 of waves 1+3 combined, and CXO using the 1:1

---

## Tips for Recognising Impulse Waves (Shane's Guide)

1. **Wave 2** is usually steep — the retracement looks quite sharp and strong

2. **Wave 3** is very easy to recognise — almost always increased volume, gaps, bullish technical indicators. Looks very sharp and strong with a high slope. The centre of wave 3 seems to have "vertical" signs

3. **Wave 4** makes a shallow retracement compared to wave 3. Seems to take longer, and the retracement is not as deep or strong as wave 2

4. **Wave 5** is less powerful and steeper than wave 3. Easier to find because it takes longer and moves shorter. Comes after wave 4 (the shallow, time-consuming correction)

---

## Strategy: Focus on Corrections

The strategy is NOT to trade the impulse waves directly — it's to **focus on corrective waves** (waves 2, 4, and ABC), because those are the SIGNALS that tell you when to enter for the next motive wave. Identify how corrections develop, wait for them to complete, then position for the next impulse.

"Following these corrective waves, there are always opportunities with the next Motive Waves. So our strategy is to focus on corrective waves — they will be Signals for us to trade."

# Elliott Wave — Extended Waves

*One of the impulse waves (1, 3, or 5) is almost always significantly longer than the other two. That's the extended wave. Identifying which wave is extended changes your targets, your expectations, and your entire trade plan.*

---

## What Are Extended Waves?

An extended wave is an impulse wave that is significantly longer than the other two impulse waves in the same sequence. It travels a greater distance and takes more time to complete. Extensions typically display strong, rapid price movement with high volume and have clear internal subdivisions (their own 1-2-3-4-5 within the extended wave).

Most impulse waves (~90%) have at least one extended wave. Extensions typically occur in **only one** of the three actionary subwaves. When the extension is so pronounced that its subdivisions are nearly the same size as the other four waves, you get a 9-wave sequence instead of the normal 5. In those cases, it can be difficult to identify which wave extended — but under Elliott Wave rules, a count of 9 and a count of 5 have the same technical significance.

### Which Wave Typically Extends?

| Market Type | Most Common Extension | Why |

|---|---|---|

| **Equities & Forex** | Wave 3 | Public participation — everyone recognises the trend and piles in. Highest volume, most vertical |

| **Commodities** | Wave 5 | Supply/demand dynamics, speculative demand, blow-off tops. Gold, silver, lithium, uranium all tend to have extended wave 5s |

| **Emerging Tech / Low Market Cap** | Wave 1 | Rare. Explosive initial move — new technology, very low market cap, massive fundamental shift. Bitcoin's early moves are a good example |

---

## The Three Cardinal Rules Still Apply

Every rule from standard impulse waves applies to extended waves AND their internal subdivisions. You need to verify rules at BOTH levels:

1. Wave 2 cannot retrace beyond wave 1's start — in the big picture AND within the extension

2. Wave 3 cannot be the shortest — in the big picture AND within the extension

3. Wave 4 cannot overlap wave 1 — in the big picture AND within the extension (exception: diagonals)

---

## Wave 1 Extension

**Rarity:** Least common. Typically seen in emerging technologies (Bitcoin, new IPOs), very low market cap situations, or major fundamental shifts that cause an immediate explosive move.

**What it looks like:** 9 sub-waves making up wave 1, then relatively short waves 3 and 5 of equal length.

**Fibonacci rules:**

- If wave 1 is extended, waves 3 through 5 combined are often **61.8-78.6%** of wave 1's length (less than 1:1 — if it were 1:1, that wave would also be extended)

- Waves 2 and 4 are very likely to be **shallow** (23.6-38.2% — bull flag territory)

- Wave 2 often ends at the level of the **internal wave 4 of wave 1** (doesn't retrace below the sub-wave 4 within the extension)

- If wave 2 retraces more than 78.6% of wave 1, the extended wave 1 count becomes doubtful — possibly just an ABC instead

---

## Wave 3 Extension

**Frequency:** Most common extension in equities and forex. This is your public participation phase — the heart of the trend.

**What it looks like:** Wave 3 has clear internal subdivisions (its own 1-2-3-4-5), is the most vertical portion of the chart, has the highest volume, and often shows gaps and bullish technical indicators. The centre of wave 3 looks nearly vertical.

**Fibonacci targets for the extended wave 3:**

- **1.618 of wave 1** — minimum for it to be considered an extension (~60-70% of the time)

- **2.0 of wave 1** — strong trends

- **2.618 of wave 1** — very strong trends

- **3.618-4.618** — extreme cases (rare but happens)

**Other relationships when wave 3 extends:**

- **Wave 5 ≈ Wave 1** — the most important rule. If wave 3 is extended, waves 1 and 5 tend to be equal in length. This is your wave 5 target

- Wave 5 can also be approximately 61.8% of wave 3

- Waves 2 and 4 typically retrace **23.6-38.2%** of the preceding wave (shallow — strong trend means dips get bought quickly)

- Wave 4 often ends near the level of the **internal wave 4 within the extended wave 3** (not the big-picture wave 4 of wave 1)

**After the impulse completes:** The subsequent ABC correction will typically return to the territory of the extended wave 3 (i.e. the correction targets the area within the wave 3 extension).

---

## Wave 5 Extension

**Frequency:** Second most common overall. Most common in **commodities** (gold, silver, lithium, uranium) due to their cyclical nature and speculative demand.

**What it looks like:** 9 sub-waves making up wave 5. It just keeps going up day after day — "these are the ones you wish you had in your portfolio." Waves 1 and 3 are normal (not extended). Often accompanied by divergence on momentum indicators early on, but then the divergence gets invalidated because the move is so powerful.

**The blow-off top:** Wave 5 extensions characteristically end in a blow-off top — rapid, unsustainable price increase followed by a sharp reversal. After the blow-off top, price can drop 20-30%+ in a single day. You do NOT want to be holding bags when a wave 5 blow-off ends.

**Fibonacci targets for the extended wave 5:**

- **1.618 to 4.618** of the total distance from the start of wave 1 to the end of wave 3

- To draw: Fib extension from wave 1 start → wave 3 end → wave 4 end → project forward

**After the impulse completes:** The correction after a wave 5 extension is typically severe. At minimum it returns to the territory of the wave 4 (within the extension), but often it retraces much further — sometimes wiping out the entire impulse move.

**Commodities and divergence:** In commodities with very extended wave 5s, divergence that appeared between waves 3 and 5 gets eventually **invalidated** because the wave 5 extension runs so hard. This is why divergence on its own isn't enough — you always need the change of market structure to confirm.

---

## Extensions Within Extensions

Extensions can nest inside each other. In equities, the third wave of an extended third wave is often also extended — this is called **"the third of the third."** It's the most powerful, vertical section of the entire move.

In commodities, you can get a **fifth wave extension of a fifth wave extension** — the blow-off top within the blow-off top.

Sometimes you won't see the deeper subdivisions on the daily chart, but you'll find them on the hourly or 4-hour chart. The extension within the extension doesn't need to be visible on every timeframe.

---

## Shane's Counting Secret — When Your Count Breaks the Rules

When you're counting and your wave 3 appears to be the shortest or your wave 4 overlaps wave 1, **don't panic — relabel as an extension:**

**Incorrect count:** Wave 1 up, wave 2 down, wave 3 up (but shorter than 1), wave 4 down (overlapping wave 1), wave 5 up → RULES BROKEN

**Correct relabelling:** What you labelled as waves 1 through 5 is actually just waves (1) and (2) of a larger extended wave 3. The "wave 3" you identified is actually just the start of the extension's internal count.

"Don't hesitate to get into the habit of labelling the early stages of third wave extensions." When your count doesn't work, the answer is almost always that you're inside an extension and need to adjust your degree.

**Key insight:** The corrective waves within an extension (sub-waves 2 and 4) tend to be **smaller** than the corrective waves of the original impulse. If sub-wave 2 of the extension is larger than the main wave 2, it's less common but not impossible — no rules are broken, it's just unusual.

---

## Practical Tips

**Use line charts when the candles are confusing.** Switch from candlestick to line chart to see the wave structure more clearly. The waves become much easier to identify.

**Start by finding the obvious waves first.** Don't try to count from wave 1 upward. Instead, find wave 2 (the deepest retracement) and wave 4, then look for divergence between waves 3 and 5. Build your picture from the anchor points outward.

**Channels for extensions:**

- **Base channel:** Wave 1 end → wave 2 end, with a parallel from the wave 1 start. A break above this channel confirms wave 3 is underway

- **Trend channel:** Wave 1 end → wave 3 end, with a parallel from wave 2. Helps identify wave 4 targets and wave 5 projections

**Ideal retracement zones:**

- Wave 2: **50% to 78.6%** (deep)

- Wave 4: **23.6% to 50%** (shallow)

- These zones help confirm your count and set targets

**Motive waves = 20% of the work, corrections = 80%.** Impulses and extensions are the relatively easy part of Elliott Wave. Corrections are where it gets complex (zigzags, flats, triangles, combinations). The course spends most of its remaining time on corrections.

**One big wave**. If you have an extended wave, you usually won't have another etended wave as most of the "power" will have been used up by the extension and the next waves will usually be shorter then normal.

# Elliott Wave — Diagonal Waves

*The second type of motive wave. Unlike impulses, diagonals allow wave 4 to overlap wave 1 — the one exception to the golden rule. They form wedge-shaped patterns and always appear at the BEGINNING or END of a move, never the middle.*

---

## What Are Diagonals?

Diagonals are wedge-shaped five-wave patterns that belong to the motive phase (they move in the direction of the primary trend), but they are NOT impulse waves. The key distinction: **wave 4 is allowed to overlap wave 1** in a diagonal. This is the only time that overlap rule is broken.

If you're counting and see a five-wave structure with overlap between waves 1 and 4, don't panic — it's probably a diagonal, not an invalid impulse count.

### Where Can Diagonals Appear?

Diagonals either **begin** something or **end** something. They cannot appear in the middle of a move.

| Type | Position | What It Signals |

|---|---|---|

| **Leading Diagonal** | Wave 1 of an impulse, or Wave A of a zigzag | Beginning of a new trend |

| **Ending Diagonal** | Wave 5 of an impulse, or Wave C of a correction | End of a trend / exhaustion |

You can also get a diagonal on the wave 5 WITHIN a larger wave (e.g. wave 5 of wave 3), but the principle holds — it's ending that sub-wave.

---

## Two Shapes: Contracting vs Expanding

**Contracting diagonal:** Widest at the start, narrowest at the end — looks like a **falling/rising wedge.** Wave 1 is the longest, wave 5 is the shortest. The more common type.

**Expanding diagonal:** Narrowest at the start, widest at the end — looks like a **crocodile mouth** or megaphone. Wave 1 is the shortest, wave 5 is the longest. Less common but powerful.

---

## Internal Structure

Each wave within a diagonal can subdivide as either:

- **3-3-3-3-3** (each wave is a three-wave ABC structure) — more common

- **5-3-5-3-5** (actionary waves are five-wave impulses, corrective waves are three-wave) — less common

Both are valid. The 3-3-3-3-3 pattern means every sub-wave within the diagonal is corrective in nature (ABC, ABC, ABC, ABC, ABC), which is why diagonals look choppier and less impulsive than standard impulse waves.

---

## Contracting Diagonal Rules

### Leading (Wave 1 or Wave A)

| Rule | Description |

|---|---|

| Wave 1 is the longest | Sets the size — everything after is smaller |

| Wave 3 can't be the shortest | Same as standard impulse rule |

| Wave 5 must be the shortest | Because wave 1 is longest and wave 3 can't be shortest → wave 5 is shortest |

| Wave 2 can't go past wave 1's start | Standard rule |

| Wave 3 breaks past wave 1's end | This is the overlap — wave 3 enters wave 1 territory (allowed in diagonals) |

| Wave 4 usually breaks past wave 1's end | More overlap — normal for diagonals |

| Wave 5 can truncate | Wave 5 may fail to surpass wave 3 |

| Wave 2 can't be a triangle | Internal structure rule |

**After a leading diagonal completes:** Expect a correction (wave 2 or wave B), then a powerful wave 3 or wave C in the same direction. Leading diagonals are the beginning of something — often something big.

### Ending (Wave 5 or Wave C)

Same structural rules as the leading version, but it appears at the END of a move. After an ending contracting diagonal completes, expect a **sharp reversal** in the opposite direction — the entire trend is exhausted.

---

## Expanding Diagonal Rules

### Leading (Wave 1 or Wave A)

| Rule | Description |

|---|---|

| Wave 1 is the shortest | Opposite of contracting — starts small |

| Wave 3 can't be the shortest | Standard rule — and wave 3 is longer than wave 1 but shorter than wave 5 |

| Wave 5 is the longest | The final wave is the biggest push |

| Wave 2 can't go past wave 1's start | Standard rule |

| Wave 4 can't go past wave 2's end | Keeps the expanding structure valid |

| Wave 4 is longer than wave 2 | Corrections get bigger as the pattern expands |

| Wave 5 always ends beyond wave 3 | No truncation allowed — wave 5 must be the longest |

| Wave 5 can overshoot or undershoot the trendline | These are called throw overs |

**Expanding leading diagonals are considered riskier** than contracting ones, but when they work, they signal the start of a major move.

### Ending (Wave 5 or Wave C)

Same expanding structure but at the END of a move. After completion, expect a sharp reversal of the entire preceding trend.

---

## Jesse Livermore's Accumulation Cylinder

The expanding leading diagonal is the same pattern Jesse Livermore called the **accumulation cylinder** — one of the earliest technical analysis concepts. Livermore identified this expanding wedge shape at the beginning of major trends: wave 1 (small), wave 3 (bigger), wave 5 (biggest) → then the breakout into wave 3 of the larger degree.

**Apple on the monthly chart** is one of the most famous examples — an expanding leading diagonal formed wave 1 before the stock went on its massive multi-year run. The S&P 500's historical yearly chart shows the same pattern at the start of the secular bull market.

If you ever see that crocodile mouth pattern at the start of a move, it could be the beginning of something very powerful.

---

## Throw Overs

A throw over occurs when wave 5 of a diagonal **briefly pushes beyond the trendline** connecting waves 1 and 3 (in a contracting diagonal) or waves 2 and 4, before reversing dramatically.

**Three outcomes for wave 5 at the trendline:**

1. **Falls short** (truncation) — doesn't reach the trendline

2. **Touches** the trendline — standard completion

3. **Goes beyond** the trendline — throw over

### Throw Over Characteristics

- After a throw over, price **reverses dramatically** back in the opposite direction and reverts quickly to where the diagonal began

- The reversal can take **one-third to one-half the time** it took for the diagonal to form — so if the diagonal took 6 months, the reversal can happen in 2-3 months

- In a **leading diagonal** throw over: the reversal is simply wave 2 (or wave B), followed by a powerful wave 3 continuing in the original direction

- In an **ending diagonal** throw over: the reversal is a major ABC correction of the entire preceding impulse — this is the big one

**Bear market example:** A falling wedge (contracting ending diagonal) with a throw under — price breaks below the wedge, triggers stop losses on everyone buying the falling wedge, then reverses sharply back up through the entire pattern. Classic stop-loss hunt before the real reversal.

---

## Real Chart Examples

**Bitcoin COVID bottom:** Leading contracting diagonal formed the base → wave 1, 2, 3, 4, 5 with overlap → ABC correction → then wave 3 took off massively

**Bitcoin top (2021):** Ending diagonal at the top of the entire move → wave 1, 2, 3, 4, 5 with overlap in a rising wedge → followed by the bear market correction

**Bitcoin also had** an ending diagonal in the C wave of the correction — same pattern but within the corrective phase, ending the C wave before the next impulse up

**South32:** Expanding leading diagonal → wave 1 smallest, wave 5 longest → crocodile mouth → then correction and takeoff

**Apple monthly:** Expanding leading diagonal formed wave 1 of the entire secular trend → one of the most famous examples in markets

**S&P 500 yearly (log):** Expanding leading diagonal at the very beginning of the long-term bull market → deep wave 2 retracement (786) → then the massive wave 3 followed

---

## Quick Reference

| Feature | Contracting | Expanding |

|---|---|---|

| Shape | Wedge narrowing to apex | Crocodile mouth widening |

| Wave 1 | Longest | Shortest |

| Wave 5 | Shortest | Longest |

| Truncation | Possible on wave 5 | Not possible (wave 5 must be longest) |

| Throw overs | Can happen | Can happen |

| More common? | Yes | No (but more powerful when it appears) |

| Where found | Leading (wave 1/A) or Ending (wave 5/C) | Leading (wave 1/A) or Ending (wave 5/C) |

# Elliott Wave — Corrections: Zigzags

*Moving from the motive phase to the corrective phase. Corrections are where Elliott Wave gets hard — 80% of the difficulty. Zigzags are the first and most common corrective pattern.*

---

## The Corrective Phase — Overview

The complete Elliott Wave cycle is 8 waves: five motive (1-2-3-4-5) + three corrective (A-B-C). Everything covered so far — impulses, extensions, diagonals — was the motive phase. Now we unpack how markets correct.

### Critical Misconception: Waves A and C Are Impulse Waves

Most people don't realise that **waves A and C are impulse waves.** They must subdivide into five waves and follow ALL the same rules as waves 1, 3, and 5 (wave 2 can't retrace past wave 1, wave 3 can't be shortest, wave 4 can't overlap wave 1 — unless it's a diagonal). They can also be extended or form diagonals.

Only **waves 2, 4, and B** are corrective waves (moving against the prevailing trend).

This is important because when price drops in five waves (not three), it's likely a wave A — not just a pullback. If it only drops in three waves, it's probably corrective within the trend. **Fives = impulse direction. Threes = corrective.**

The one exception: leading diagonals can move in waves of three (3-3-3-3-3), which can look corrective but are actually motive. That's what makes them tricky in real time.

---

## Zigzag Correction (5-3-5)

A zigzag is a sharp three-wave corrective pattern labelled A-B-C, structured as **five-three-five:**

- **Wave A:** Five waves down (impulse or diagonal) — the initial drop

- **Wave B:** Three waves up (any corrective structure — flat, triangle, zigzag, complex) — the counter-trend bounce

- **Wave C:** Five waves down (impulse or diagonal) — the final leg that completes the correction

If the structure isn't five-then-three-then-five, it's not a zigzag.

### Key Characteristics

- Zigzags are the **sharpest** type of correction — quick, decisive moves

- Most common corrective pattern and the easiest to identify and trade

- Wave C is typically **at least as large as wave A**, often extends to 1.618 or beyond

- Waves A and C can contain extensions and can form as diagonals (ending diagonals on wave C are common)

---

## Fibonacci Targets for Wave C

Use the **trend-based Fib extension tool:** click from the start of wave A → end of wave A → end of wave B → project forward.

| Ratio | Description | Frequency |

|---|---|---|

| **1:1** | Wave C equals wave A in length — "partner leg" | Most common |

| **1.272** | Slight extension beyond wave A | Common |

| **1.618** | Wave C = 1.618 × wave A — stronger correction (golden ratio) | Very common |

| **0.618** | Wave C shorter than wave A — more common when wave B is shallow (e.g. triangle) | Less common |

| **2.0** | Significant extension | Uncommon |

| **2.618** | Extreme extension — really powerful bear moves | Rare (tech bubble, major crashes) |

**Rule of thumb:** Always check the 1:1 first, then the 1.618. These are your two primary targets. If wave B was a shallow correction (like a triangle), the 0.618 becomes more probable for wave C.

### Real Examples

- **Bitcoin 2013-2015 bear market:** Wave C hit the 1.618 extension ($198 bottom)

- **Bitcoin 2011 correction:** Wave C hit the 1:1 — equal to wave A

- **Ethereum:** Three separate corrections all bottomed at the 1.618 — "Ethereum loves a 1.618"

- **Apple GFC (2008):** Zigzag correction, wave C hit 1.618, with an ending diagonal forming the final leg of wave C

- **Apple tech bubble:** Extreme bear market — wave C extended to the **2.618** with an ending diagonal at the bottom

- **Bitcoin COVID correction:** Wave C hit the 1.272

---

## ABC Personality — What Each Wave Feels Like

Understanding the psychological character of each wave helps you confirm your wave count. If the sentiment doesn't match, your count might be wrong.

### Wave A — "It's Just a Pullback"

- Fundamental news is still positive

- Most analysts see it as a healthy correction in a still-active bull market

- Market structure hasn't broken yet — technically could still be just another higher low

- Volume increases on the drop, implied volatility rises

- People who know charts start to exit, but the majority holds

- **"Just a dip, buy it like the last one"**

### Wave B — "Told You So"

- Prices reverse higher — seen as resumption of the bull trend

- This is the **right shoulder** of a head & shoulders pattern in classical TA

- Volume during wave B should be **lower than wave A** (weak bounce)

- Fundamentals haven't turned negative yet but aren't improving

- Everyone who held through wave A feels vindicated: **"See? I told you it was just a pullback, you idiot bears"**

- This is the fake-out — people assume the trend will continue like it always has

### Wave C — "Oh No"

- Prices drop **impulsively** in five waves — sharp and rapid

- Volume picks up significantly

- By wave 3 of wave C (the middle of the drop), almost everyone realises a bear market is entrenched

- Fear enters the market — sentiment flips bearish

- Wave C is typically at least as large as wave A, often extends to 1.618 or beyond

- People who held through wave A and wave B are now so deep in losses they can't bring themselves to sell — they start wishing they'd sold on the first drop

- **If you haven't got fear in the market yet, you're probably not in wave C**

### Matching Sentiment to Wave Count

- Calling five waves up but no exuberance/euphoria? → You might not actually have five waves up

- Calling a completed ABC but no fear? → The correction might not be done

- Wave A can sometimes trigger extreme bearishness too (especially if wave A itself has an extended wave 5) — which then gets faded by the wave B bounce

---

## The Distinction: Corrective or Impulsive?

The hardest question in real time: is this move corrective (ABC about to end) or impulsive (wave 1-2 of a new trend)?

**After a zigzag completes:** You don't know if you're getting wave 3 in the same direction (it was just a correction within the trend) or if the ABC was the entire correction and the trend resumes.

**How to tell:**

- If price then moves in five waves beyond the correction → it's impulse, the trend is resuming

- If price moves in three waves → it might be another corrective structure (W-X-Y, flat, etc.)

- Wave 4 can't enter wave 1 territory — if it does, your impulse count is invalid

- **This is why you always look to take profit in the zag zone** — because at the zag zone you don't know if it's wave 3 or wave C

---

## Zigzags in Both Directions

**Bullish zigzag (in a bear market correction):** Five waves UP for A, three waves DOWN for B, five waves UP for C — a sharp rally within a larger downtrend.

**Bearish zigzag (after a bull market impulse):** Five waves DOWN for A, three waves UP for B, five waves DOWN for C — the standard correction after a five-wave advance.

The structure, rules, and Fibonacci relationships are identical regardless of direction.

---

## What's Coming Next

Zigzags are just the first type of correction. Still to come:

- **Flats** (3-3-5 structure) — sideways corrections where wave B retraces most or all of wave A

- **Triangles** (3-3-3-3-3) — converging patterns that appear in wave 4 or wave B

- **Complex corrections** (W-X-Y, double/triple zigzags, combinations) — when simple corrections aren't enough

Corrections are where multiple possible counts exist simultaneously. Even experienced Elliotticians run 4-5 different scenarios during corrections and narrow down as the pattern develops. Impulses = relatively easy. Corrections = years of practice.

# Elliott Wave — Corrections: Flats

*The second type of correction. Where zigzags are sharp and fast, flats are sideways and time-consuming. Two different ways the market capitulates people — fear (zigzags) or boredom (flats).*

---

## Sharp vs Sideways Corrections

The market spends **80% of its time in corrections.** Corrective patterns are time-consuming and their complexity increases as they unfold. If you can spot the END of a correction, your market timing improves dramatically.

| Type | Examples | How It Capitulates |

|---|---|---|

| **Sharp** | Zigzags, double/triple zigzags | Fast, violent drops — people panic sell |

| **Sideways** | Flats, triangles | Drawn out over weeks/months/years — people get bored and move their money elsewhere |

A sharp correction might take 10 candles to play out. A sideways correction can take 50+ candles. The most famous flat correction in history (S&P 500 tech bubble → GFC) played out over **10 years.**

---

## What Is a Flat Correction?

A flat is a three-wave corrective move labelled A-B-C, structured as **3-3-5:**

- **Wave A:** Three waves (any corrective pattern EXCEPT a triangle — can be zigzag, flat, double three, etc.)

- **Wave B:** Three waves (any corrective pattern — usually a zigzag, but can include triangles)

- **Wave C:** Five waves (impulse or ending diagonal) — always motive

### How to Distinguish Flat from Zigzag

| Feature | Zigzag | Flat |

|---|---|---|

| Structure | 5-3-5 | 3-3-5 |

| Wave A | Five waves (impulse) | Three waves (corrective) |

| Speed | Sharp and fast | Sideways and slow |

| Depth | Deep retracements (618+) | Shallow retracements (236-382) |

**Key identification trick:** If wave B moves up in three waves (not five), look back — did wave A also move in three waves? If yes, you're probably getting a flat correction and wave C (five waves) is coming. Threes followed by threes = flat incoming.

---

## Three Types of Flat Corrections

### 1. Regular Flat

Wave B retraces **at least 90%** of wave A (but doesn't exceed wave A's start). Wave C ends at or slightly past wave A's end. Produces a sideways, range-bound appearance — roughly equal highs and equal lows.

**Fibonacci relationships:**

- Wave B = minimum 90% of wave A (must reach at least 90% to qualify)

- Wave C = 61.8%, 100%, or 123.6% of wave A

**Flat corrections are typically shallow** in the context of the larger trend — they tend to retrace to the Fib 236 or 382 of the preceding impulse. Rarely do they reach the 618. The trend is strong enough that it just needs time to consolidate before continuing.

**Famous example:** S&P 500 from 2000-2009 — wave A (tech bubble crash), wave B (2003-2007 recovery that almost reached the old highs), wave C (GFC crash that took out the lows). Played out over a decade. The wave B tricked everyone into thinking the bull market was back, then wave C fell off a cliff.

### 2. Expanded Flat (Irregular)

Wave B extends **beyond** the start of wave A (takes out the high in a bull market correction). Wave C then extends **substantially beyond** the end of wave A (takes out the low). This is the **liquidity hunter** — it gets everyone on both sides.

**The trap:** Wave B breaks to new highs → everyone goes long (change of market structure!) → then wave C reverses and stops them all out below the lows. "Put your entry where their stop loss is."

**Fibonacci relationships:**

- Wave B = **1.236 to 1.382** of wave A (the "pocket zone" — where wave B typically reverses)

- Wave C = **1.618 to 2.618** of wave A (measured from start of A to end of A, projected from end of B)

**Wave C should show momentum divergence.** When you see divergence on the C wave, the correction is likely ending.

**Bitcoin example:** Five waves up → wave A down → wave B up into the 1.272-1.382 pocket zone → wave C down to the Fib 2.0. Perfect expanded flat before continuation.

### 3. Running Flat

Wave B extends beyond the start of wave A (same as expanded flat — takes out the high). But wave C **fails to reach** the end of wave A (doesn't take out the low). The correction stays shallow — extremely bullish signal.

**In a bull market:** Takes out the high, doesn't take out the low.

**In a bear market:** Takes out the low, doesn't take out the high.

**Fibonacci relationships:**

- Wave B = **1.236 to 1.382** of wave A (same pocket zone as expanded flat)

- Wave C = **61.8%** of wave A is the key golden ratio target (often falls short of wave A's end)

Wave C should still show momentum divergence. The moment wave C goes beyond wave A's end, it can no longer be a running flat — it becomes an expanded flat instead.

**S&P 500 example:** Leading diagonal for wave 1 → running flat correction → wave B hit the 1.272 perfectly → wave C came down to approximately 1:1 but didn't take out the low → trend continued higher.

---

## Quick Comparison

| Feature | Regular | Expanded | Running |

|---|---|---|---|

| Wave B vs Wave A start | Doesn't exceed (90%+ retrace) | Exceeds (1.236-1.382) | Exceeds (1.236-1.382) |

| Wave C vs Wave A end | At or slightly past | Substantially past | Falls short |

| Takes out highs? | No | Yes | Yes |

| Takes out lows? | Sometimes slightly | Yes (substantially) | No |

| Bullish implication | Neutral — sideways | Bearish trap first | Most bullish — shallow correction |

| Common name | — | Liquidity hunter | — |

---

## Identifying Flats — Practical Tips

- **If wave A moves in three waves** (not five) → it's a flat, not a zigzag. Look for wave B to also be three waves, then wave C to be five waves

- **Flat corrections are shallow** in the larger trend context — typically Fib 236 to 382 retracements. If you're seeing 618+ retracement, it's more likely a zigzag

- **Wave C is always impulsive** — sharp, fast, five waves. Even in a boring sideways flat, wave C drops (or rises) rapidly. "C waves fall off a cliff"

- **Wave C should have divergence** — especially in expanded and running flats, look for momentum divergence on wave C to confirm the correction is ending

- **If you're struggling to count waves** — drop to a lower timeframe to see the subdivisions more clearly. Flats play out on every timeframe, from 1-minute to yearly

- **Once you learn to see them, you'll see them everywhere** — the educator demonstrated running flats, expanded flats, and regular flats all on the same chart within different sections

# Elliott Wave — Corrections: Triangles

*The third type of correction. Five-wave sideways pattern labelled A-B-C-D-E. Triangles only appear in one specific position — and that fact alone makes them one of the most useful predictive tools in Elliott Wave.*

---

## What Are Triangles?

Triangles are corrective five-wave patterns bound by converging or diverging trend lines, labelled **A-B-C-D-E** (letters, not numbers — because they're corrective). Each sub-wave is itself a corrective structure (typically zigzags), producing a sideways consolidation that gets progressively tighter.

Triangles are a **sideways correction** — they capitulate through time and boredom, not through sharp price drops.

---

## Where Triangles Can Appear — The Golden Rule

Triangles **always occur in the position prior to the final actionary wave.** They can ONLY appear in:

- **Wave 4** of an impulse (before the final wave 5)

- **Wave B** of a zigzag (before the final wave C)

**Triangles CANNOT appear in wave 2.** This is incredibly useful for predictive analysis:

- If you see a first move followed by a triangle → you're NOT in an impulse. You're in a correction (ABC), and all you're getting is a partner leg (wave C) before the correction ends

- If you see a triangle after three impulse waves → it's wave 4, and wave 5 (the final push) is coming

- After the triangle breakout, you know it's the LAST move in that direction before a major correction of the entire impulse

**"Whenever you see triangles, make sure you're taking profits at the end of them."**

---

## Three Types of Triangles

### 1. Contracting Triangle (Symmetrical)

Both trend lines converge — widest at the start, narrowest at the end. Each wave is progressively smaller and more contained. The most common type.

### 2. Barrier Triangle (Ascending / Descending)

One side is flat (horizontal support or resistance), the other side converges toward it. This is the ascending triangle (flat top, rising lows) or descending triangle (flat bottom, lower highs) you already know from classical TA — they're actually Elliott Wave barrier triangles.

The flat boundary represents supply or demand that gets repeatedly tested. Each test eats away at that supply/demand until it finally breaks through.

### 3. Expanding Triangle

Trend lines diverge — narrowest at the start, widest at the end. Less common.

**Running triangle:** A variation of the contracting triangle where wave B exceeds the start of wave A (takes out the high/low). Similar concept to a running flat — extremely bullish/bearish signal.

---

## The Inner Waves (A through E)

Each wave subdivides into a corrective three-wave pattern. ~90% of the time they're zigzags.

### Wave A — "Just a Normal Correction"

- Sharp move against the trend (zigzag) — sets the initial boundary

- Nobody knows it's a triangle yet. Everyone thinks it's a standard ABC correction

- Comes down to the golden pocket (382-618) of the preceding trend

- People expect an ABC and continuation

### Wave B — "We're Back On"

- Counter-move retracing a significant portion of wave A (typically 38.2-61.8% of wave A)

- People think the trend is resuming — change of market structure

- Does NOT surpass the flat boundary significantly in barrier triangles

- Now you have: impulse → correction → continuation. Looks like a normal trend

### Wave C — "Wait, What?"

- Moves back down, surprising those who thought the trend resumed

- Smaller than wave A (in contracting triangles)

- Cannot exceed the end of wave A (otherwise it's not contracting)

- Often retraces 61.8-100% of wave B

- People start thinking: double top? Running flat? The count gets confusing

### Wave D — "Maybe We're in a Triangle"

- Counter-move back up — shorter and weaker than wave B

- Does NOT reach beyond wave B's starting point (in contracting triangles)

- **This is the first moment you can start to identify the triangle** — you now have two points on each side to draw converging trend lines

- Running flat theory dies here because there aren't five waves down

- People start drawing triangle formations

### Wave E — "Final Consolidation"

- Final wave, moves opposite to wave D — typically short and shallow

- Usually does NOT reach wave C's level

- Can end anywhere between the converging trend lines

- Marks the completion of the pattern — breakout imminent

- **Wave E is the ONLY sub-wave that can itself be a triangle** — creating a 9-wave triangle (4 zigzags + 1 triangle within wave E). This extends and drags out the consolidation even further

---

## Triangle Characteristics

**Volume:** Diminishes progressively as the triangle forms — reflecting indecision. Upon breakout from wave E, volume surges, confirming resumption of the primary trend.

**Alternation:** Waves alternate between sharp and choppy. If wave A is a sharp zigzag, wave B might be more corrective and drifting. Wave C sharp again, wave D more relaxed.

**The Thrust:** After a wave 4 triangle completes, wave 5 often moves quickly and covers a distance similar to the triangle's widest part. Elliott called this the "thrust." It's usually an impulse but can be an ending diagonal. In strong markets, wave 5 after a triangle can be an extended fifth — the blow-off top.

**Buyers/sellers converging:** In an ascending triangle, buyers are stepping in at progressively higher levels (higher lows). In a descending triangle, sellers are stepping in at progressively lower levels (lower highs). The flat boundary is supply/demand being eaten away until it breaks.

---

## Triangle Within a Triangle

Wave E can itself be a triangle, extending the pattern to 9 waves total (A, B, C, D, then a-b-c-d-e within wave E). This is how triangles get really drawn out.

**Bitcoin bear market example (April-November 2018):** Waves A, B, C, D were standard zigzags. Then wave E itself became a triangle (a-b-c-d-e), dragging the entire consolidation out to 6 months. The pattern was: zigzag, zigzag, zigzag, zigzag, triangle. Nine waves total before the final breakdown.

---

## How People Get Fooled at Each Stage

| Wave | What People Think | Reality |

|---|---|---|

| A | "Normal pullback, buy the dip" | First leg of the triangle |

| B | "Trend is back! Change of market structure!" | Just a corrective bounce |

| C | "Double top? Running flat? Five waves down coming?" | Nope — only three waves, then reversal |

| D | "OK this is weird... maybe a triangle?" | First time you can identify the pattern |

| E | "Is it going to break out or break down?" | Final consolidation before the thrust |

---

## Practical Trading Tips

- **After a triangle breakout, it's the LAST move.** Trade it for profit but have your exit planned — wave 5 after a triangle leads to a correction of the entire impulse. The educator traded the SHORT after the triangle breakout on BNB — once wave 5 completed and broke back through, the entire move got corrected

- **Count five waves inside the triangle.** A lot of people who don't know Elliott Wave miscount triangles. You need A-B-C-D-E (five corrective waves, each in threes) for it to be a valid triangle

- **Triangles tell you what's coming next.** If it's wave 4 → wave 5 thrust coming, then major correction. If it's wave B → wave C coming (often sharp and fast). Either way, you know the next move is the final one

- **Use Fibonacci on the preceding impulse** after the triangle completes. Once wave 5 finishes, you're retracing the whole impulse — measure from wave 1 start to wave 5 end and look for the zag zone (382-618)